Decarbonizing the supply chain: why market-based solutions are key to meeting 2030 targets

We examine the challenges companies face in meeting near-term supply chain emissions targets amid lagging updates to major climate standards, explore best practices for applying market-based accounting approaches to supply chain decarbonization, and introduce our Supply Chain Emissions Reduction solution.

Interested in value chain decarbonization?

Learn more of the latest strategies in our Value Chain Intervention Guide.

Originally published March 25, 2025 with an addendum added September 19, 2025

The number of companies pledging to set ambitious, near-term climate targets, as defined by the Science-Based Targets Initiative (SBTi), has roughly doubled each year since 2020. While this pace of ambitious target-setting is good news for the climate, many of these companies are confronting a critical challenge as 2030 nears: conventional methods for measuring emissions and showing progress against targets often cannot fully reflect the positive impacts of mitigation actions companies undertake.

Rising pressure and key challenges in reducing supply chain emissions

To reduce supply chain emissions and advance near-term climate targets, companies are increasingly exploring ways to modify supply chain activities to result in lower emissions (see Box 1 for common terminology companies use to describe these efforts). However, typical supply chains are highly complex, often including many tiers of companies, points of product mixing, and extensive movement of goods, even across national borders. A vast majority of companies lack complete insight into their supply chain, often with lessening traceability the further upstream in the supply chain they look.

Major corporate climate action standards have yet to adapt to these complexities of modern supply chains. Specifically, prevailing guidance from the Greenhouse Gas Protocol (GHGP) and SBTi is based on a system of attributing emissions to corporate activities, and allowing companies to use broad, industry-average estimates of emissions per dollar spent or unit purchased to create these attributional inventories. However, when it comes to attributing positive mitigation impacts companies may support, this framework falls short. To report reduction or removal progress in their supply chains, companies must clear a much higher traceability bar: they must be able to document the fraction of products they physically receive from any sites where they drive mitigation impact, and then downscale claims per this proportion. This approach severely limits the impact companies can claim, weakening incentives to invest in supply chain decarbonization, as goods are often distributed across buyers at multiple supply chain tiers before reaching their final destination. Additionally, striving to establish physical traceability from intervention sites to end users creates an immense administrative burden. Rather than spending resources tracking and documenting contractual chains of custody, companies could better direct their efforts toward achieving greater decarbonization impact.

Supply chain decarbonization efforts are commonly known by various terms, including “value chain interventions,” “supply chain interventions,” “insets,” and “mitigation activities within the value chain.” At 3Degrees, we refer to them as Supply Chain Reductions (SCRs).

Avoiding the term “insets” in particular can help prevent the implication that we are solely referring to carbon credit-based structures for reducing within-value-chain emissions (as other intervention and accounting approaches exist). It also helps avoid the potential confusion and negative associations linked to the term “offsets.”

Interested in value chain decarbonization?

Learn more of the latest strategies in our Value Chain Intervention Guide.

Recognizing these limitations as well as the need to drive progress on lowering supply chain emissions, companies have been exploring ways to support and track decarbonization progress by introducing “market-based” accounting approaches (see Box 2). These market-based mechanisms would allow companies to rigorously quantify mitigation impacts they drive in the specific markets they source from, while avoiding costly and complex efforts to document fractions of goods they receive through layers of upstream suppliers. Market-based approaches can also provide clearer incentive for companies to invest in efforts to meaningfully decarbonize their sourced goods, even if their specific procurement choices may shift from year to year. GHGP has already recognized the value of this kind of approach in scope 2 emissions accounting guidance, where it allows companies to claim purchases of renewable energy in common electricity markets using market-based mechanisms even if the companies cannot prove physical receipt of every renewably produced electron.

“Market-based” accounting approaches refer to frameworks that separate the environmental attributes of goods (e.g., the lower emissions profile of a sustainably grown crop) from their physical flow. Market-based mechanisms, such as certificate or credit systems and mass-balance tracking, thereby enable companies to quantify and claim the emissions impacts they drive in their supply chains without being constrained by their ability to track a segregated volume of goods physically received from any specific upstream supplier (e.g., a specific farm).

The supply chain emission reduction challenge, illustrated

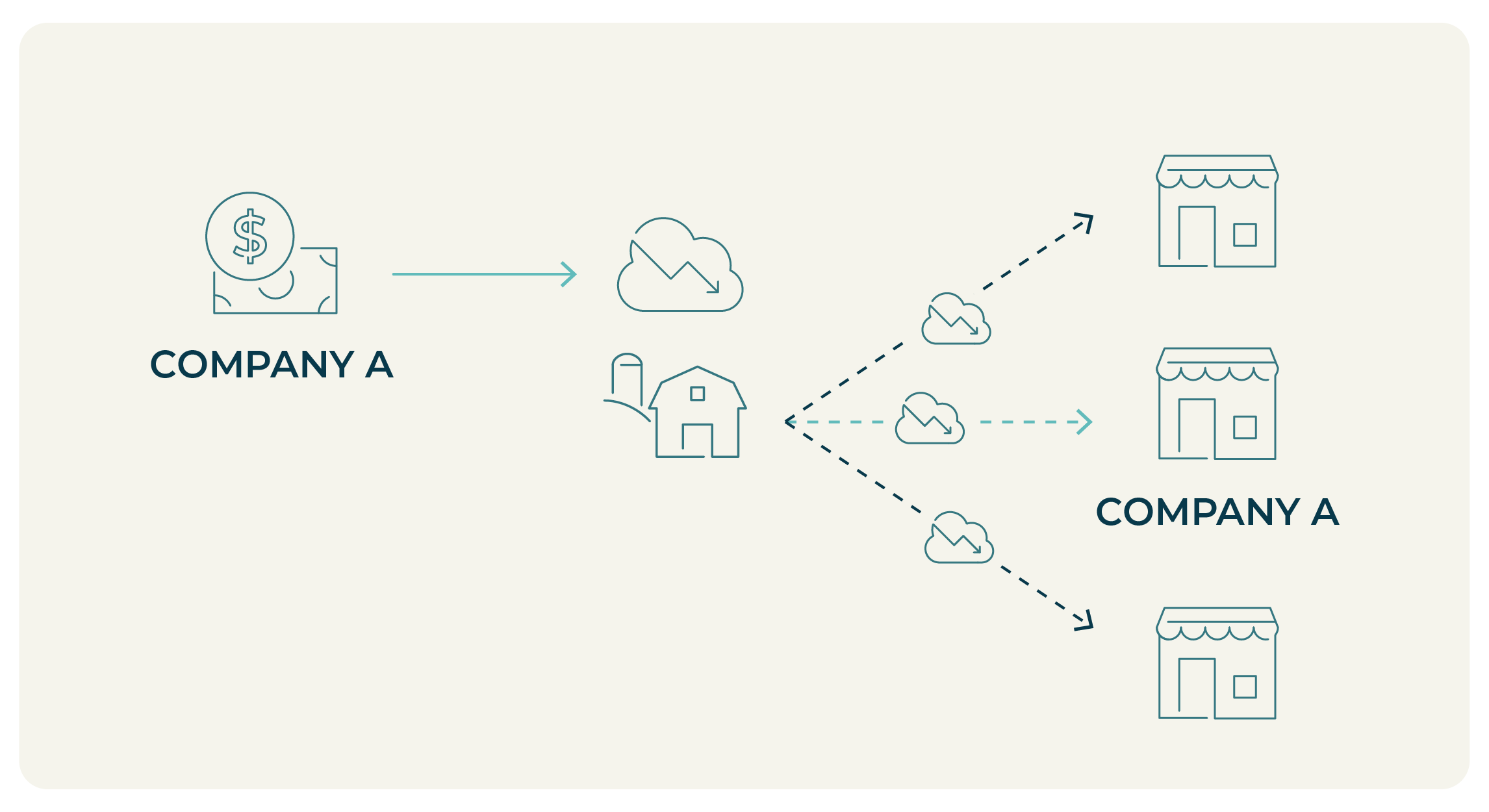

Figure 1: GHGP-aligned approach. Company A invests in the fertilizer intervention on the corn farm, but under current guidance, the resulting reductions would be dispersed among all buyers of the corn / corn products – Company A can only claim reductions in proportion to the quantity of corn it ultimately receives from the farm.

Company A is a bourbon distiller and brand with significant corn farming emissions in its supply chain. In exploring ways to reduce its supply chain emissions, Company A traces some of its corn crop back to a farm where it decides to fund an intervention optimizing fertilizer use, reducing emissions by 7,500 metric tons CO2e annually.

Under current GHGP guidance, Company A could only claim reductions proportional to the corn it purchases from the farm: e.g., if it buys 10% of the farm’s total crop, it could claim just 750 tons of reductions. In theory, the remaining reductions would be distributed to other customers of the corn farm, each making claims in proportion to the amount of goods they source from the farm. This would result in “stranded assets” for Company A, as it would be unable to claim the full impact of its investment and therefore may think twice about funding this mitigation initiative.

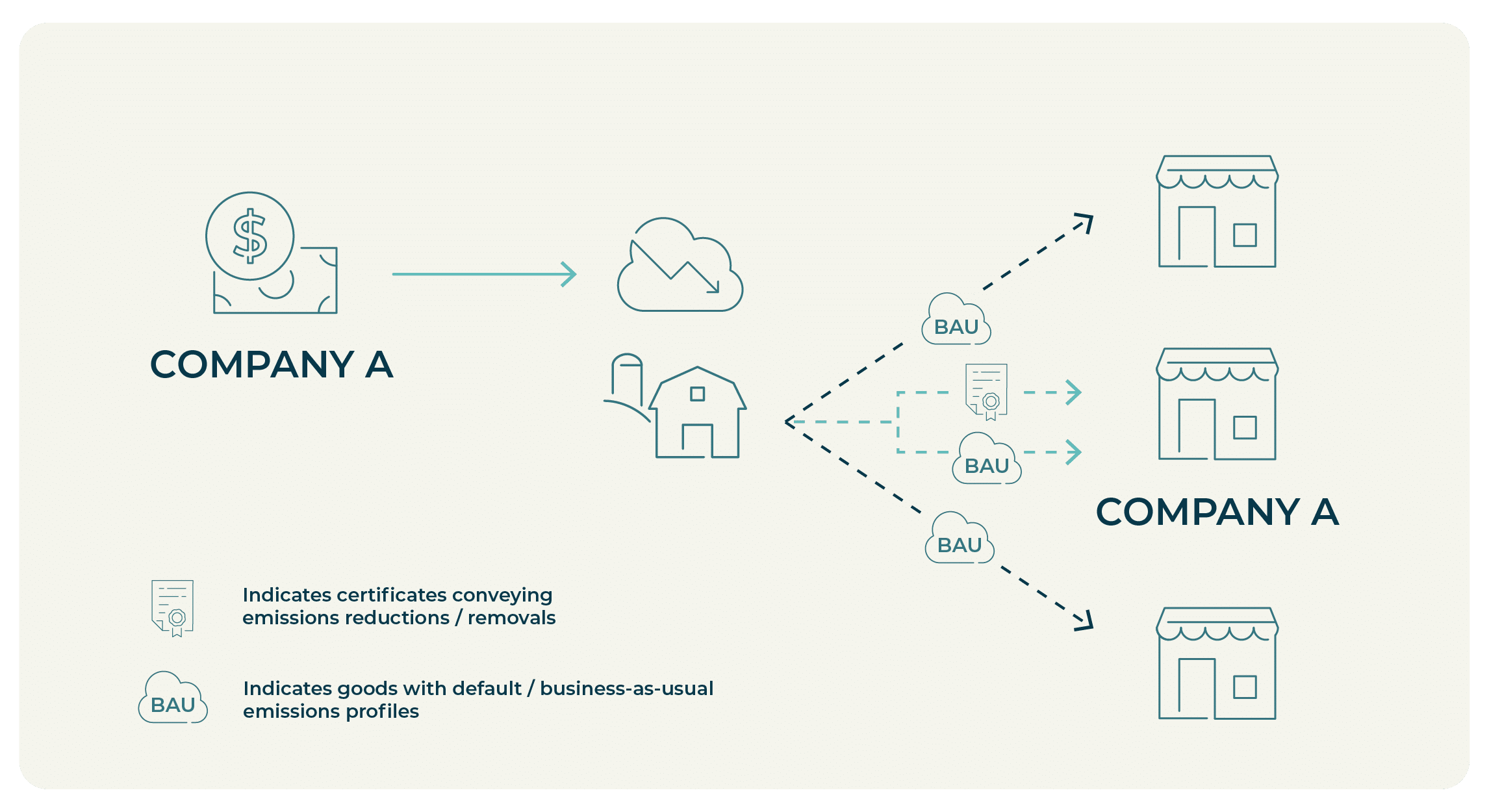

Figure 2: Scope 3 market-based mechanisms approach. Company A invests in the fertilizer intervention on the corn farm and claims the full reduction impact it caused.

A market-based approach, however, would allow Company A to claim the full 7,500 tons of reductions it drove (constrained only by the total corn volume Company A can claim to source from corn farms sending corn to the same processor, or otherwise defined to be within a common geographic market). This approach would also allow Company A to define its supply shed to better reflect realities of agricultural supply chains: for example, as a group of farms producing functionally interchangeable corn crops in a specifically defined region of Kentucky where Company A sources. Using this definition, Company A could support interventions on farms that are within a well-defined group of current, past, and potential future suppliers, offer consistent support to targeted farms over time, and ensure that progress tracking reflects real decarbonization across a market. Compared to an approach aligned with currently available guidance, this could avoid stranding assets or abruptly removing decarbonization support from farms if Company A changes its procurement from one farm to another within the same regional market.

Fortunately, both GHGP and SBTi are in the process of updating their broader guidance and have publicly stated their intention to consider the use of market-based mechanisms for supply chain decarbonization. However, finalized updates are not expected for at least three years, leaving companies in limbo. Those waiting for explicit, affirmative guidance before leveraging market-based solutions risk missing critical opportunities to make progress toward their 2030 climate targets.

SBTi’s draft update to its Net-Zero Standard, if finalized, would recognize market-based mechanisms as a way to make progress on scope 3 targets

On March 18, 2025, SBTi released a much anticipated draft revision to its Corporate Net-Zero Standard for public consultation. Among the most notable proposed changes is the introduction of a new category of recognized mitigation action, termed “indirect mitigation,” as a way for companies to demonstrate progress against scope 3 targets. (See 3Degrees’ full blog here for more detail on SBTi’s draft standard).

The draft standard revision defines indirect mitigation as “actions that contribute to net-zero-aligned transformation relevant to the company’s value chain but that cannot be traced back to activities or emissions sources within the company’s value chain.” The draft standard further clarifies that this includes mechanisms such as book-and-claim systems and potential variants of mass balance, both generally understood to be market-based approaches.

Importantly, the draft standard includes several caveats for the use of indirect mitigation:

• It should not affect a company’s GHGP-aligned emissions inventory (i.e., must be reported separately)

• It should deliver measurable outcomes, comparable to direct mitigation

• Its use must be justified (i.e., companies should be able to demonstrate why tracing mitigation impacts directly through the value chain is not feasible)

• It should be complemented by direct mitigation where relevant (e.g., sustainable aviation fuel certificate purchases should be paired with policies to reduce business travel and prioritize low-emissions travel options)

• It will count toward scope 3 targets only as an “interim measure” and will be subject to additional “quality criteria,” both of which SBTi has yet to define

Although not final, this update marks a welcome evolution in SBTi’s approach, signaling increased openness to market-based mechanisms for supply chain decarbonization. 3Degrees communicated its support for this evolution in its contribution to SBTi’s public consultation that concluded June 1, 2025, and remains optimistic that recognition of market-based mechanisms for scope 3 will appear in the finalized revision of the Net-Zero Standard.

Companies must invest in action now to achieve sufficient emission reductions by their near-term target dates. As such, 3Degrees supports the use of high-quality market-based mechanisms for supply chain emission reductions, and urges companies to act immediately rather than delay in anticipation of future guidance updates.

Many companies, especially those with large agricultural supply chains, have already begun moving forward with supply chain interventions and market-based accounting mechanisms while advocating for their recognition in guidance updates. For example, in its most recent sustainability report, Unilever stated that GHGP “will need to evolve” for Unilever to be “permitted to count the benefits” of investments already made in regenerative agriculture and lower-carbon dairy towards its near-term scope 3 target. Nestle has also taken bold steps to support removals in its agricultural sourcing regions (that is, supply sheds defined more broadly than GHGP currently allows) and is communicating about these removals as progress against its near-term scope 3 target. ,

At the same time, other companies are already leveraging market-based mechanisms for scope 3 without explicit calls for guidance to evolve. For example, a prominent non-dairy milk company is supporting regenerative agriculture practice adoption among a cohort of farmers in Canada, aiming to reduce and remove emissions on acreage equivalent to the area used for its total oats supply, but without physical traceability of oats from all its enrolled farms to its milk cartons. However, this company does not prominently acknowledge that this approach represents a divergence from GHGP guidance. Similarly, a large confectionery company recently registered an emission reduction project on a supply chain “impact unit” registry run by SustainCERT, and publicly referenced active exploration of co-funding and co-claiming impacts of agricultural decarbonization using market-based mechanisms. However, the company does not yet acknowledge use of market-based mechanisms for scope 3 in its formal reporting.

While some companies, usually those with highly sophisticated sustainability strategies, have taken bold steps to advance their scope 3 action in this uncertain time, others have been stymied by the state of guidance and are even considering reducing the ambition of their scope 3 decarbonization commitments. Specifically, some companies are considering not renewing their science-based targets unless market-based mechanisms can be used to achieve them, while others are facing hesitation from leadership to invest in decarbonization if the results may not be claimable under major guidance by 2030. These kinds of rollbacks or delays in action present a significant challenge to collective efforts to keep the world on a 1.5°C pathway.

Recognizing that market-based mechanisms will be crucial to unlock sufficient scope 3 decarbonization in the next few years, several initiatives have emerged to set forth frameworks for credible impact accounting and value chain association (i.e., how companies can define an intervention as within vs. outside their supply chains). These initiatives include the AIM Platform, the Value Change Initiative, Center for Green Market Activation, and Verra’s Scope 3 Standard. These standards’ early-stage work shows some overlap, providing potentially helpful direction to companies that have capacity to stay up to date on various developments (i.e., working group meetings, reports, case studies, webinars, and more). However, for supply chain reductions to become accessible to a greater range of companies, corporate, academic, and nonprofit thought leaders need to coalesce around general best practices and sector-specific frameworks that are both credible and widely adoptable.

As the market continues to evolve around best practices and companies await updates to guidance, we urge companies to begin investing in market-based instruments to drive supply chain decarbonization. We also recommend that companies apply the following best practices to maximize credibility and integrity of these efforts:

- Pursue emission reduction and removal projects that have rigorous quantification methodologies

- Consider partnering with a monitoring, reporting, and verification (MRV) entity to ensure intervention impacts are robustly quantified and monitored

- Internally define a minimum level of traceability (i.e., to defined “supply sheds” or “sourcing regions”) to ensure investments support emission reductions and removals within the reporting company’s supply chain. 3Degrees recommends that companies assess the most useful level of traceability data for targeting investments and driving impact, with the understanding that while data availability should not delay action, pursuing better data can provide a more accurate measurement of ongoing value chain emissions and decarbonization progress. This means companies’ traceability requirements may differ across commodities or even within single commodity supply chains (e.g., a company may find it more practical to trace milk to a specific dairy farm, compared to identifying a specific producer of fertilizer used to grow feed for those dairy cattle). In parallel, we recommend that companies continue working to collect more accurate data and expand their understanding of their supply chains.

- Internally align on a definition of causality, i.e., how the reporting company plans to demonstrate that the impacts it claims would not have occurred without its support. At a minimum, this definition should consider whether mitigation impacts were already occurring prior to the causal action, and whether they would have occurred under regulation or government-provided incentives (“regulatory additionality”).

- Ensure clear ownership / allocation of emission reductions. Specifically, companies can seek language in contracts with other project participants stating that the lower-emission profiles of goods resulting from specific investments will be allocated to the reporting company and its acknowledged partners only, avoiding double-counting.

- Consider registering measured intervention impacts with a credible registry, if feasible.

Given the ongoing complexity of supply chain interventions and the urgent need for companies to drive scope 3 decarbonization, 3Degrees has developed a solution to simplify and de-risk upstream mitigation interventions. This solution, Supply Chain Reductions (SCRs), is a credit-based mechanism under which each SCR is generated by a high-quality emission reduction project, either sourced from within a buyer’s defined value chain or developed as a bespoke project to meet specific needs. Each project’s impacts are rigorously quantified in accordance with major carbon crediting standard or scope 3 standard (e.g., the SustainCERT framework or the Verra Scope 3 Standard). In addition to this robust measurement and verification, credits are supported with proof of sourcing and ownership safeguards aligned with best practices.

SCRs are a particularly useful tool for companies with complex supply chains where traceability throughout the full supply chain may not be feasible, such as food & beverage or apparel companies with extensive agricultural sourcing needs. In the future, SCRs may also be highly useful for other sectors as well.

3Degrees urges companies to take immediate action on scope 3 decarbonization, whether through pre-packaged solutions such as SCRs, or other efforts to reduce emissions throughout the supply chain. Now is the time to act, as waiting for future guidance may jeopardize the chance to drive needed mitigation impact and meet critical near-term climate targets.

Get more information on our SCR offerings or advisory services to support use of market-based instruments for scope 3 decarbonization.

Suggested insights

Authors

Hailey Baker is a consultant on 3Degrees’ Climate Strategy consulting team.

Hailey Baker is a consultant on 3Degrees’ Climate Strategy consulting team.

Tory Hoffmeister is a manager on 3Degrees’ Climate Strategy consulting team.