Europe’s energy market: navigating negative prices and geopolitical shifts in H2 2024

Explore the impact of negative electricity prices and geopolitical shifts on Europe’s energy market in the second half of 2024.

Renewable energy strategies at your fingertips

Receive worldwide renewable energy updates directly in your inbox with our bi-annual Global Market Insights Reports.

The European energy market is experiencing notable changes driven by several trends, including the increasing frequency of negative electricity prices and the geopolitical factors reshaping energy strategies. The rising occurrence of negative electricity prices reflects the rapid expansion of renewable energy generation in certain regions, intensifying market volatility and highlighting the need for greater flexibility and infrastructure upgrades. Meanwhile, geopolitical developments—from U.S. elections to European Commission reforms —are adding layers of complexity to Europe’s energy market outlook.

To thrive in this evolving environment, energy market participants, policymakers, and grid operators must adopt proactive strategies to build resilience and capitalise on opportunities. This article delves into the core dynamics of negative pricing trends, potential solutions, and the geopolitical factors influencing the European energy market, with a particular focus on the power purchase agreement (PPA) sector.

Negative price trends in Europe

Negative electricity prices have become a regular feature of Europe’s energy markets. As renewable energy capacity surges, particularly solar and wind, oversupply during low-demand periods leads to an increasing number of zero or negative price hours.

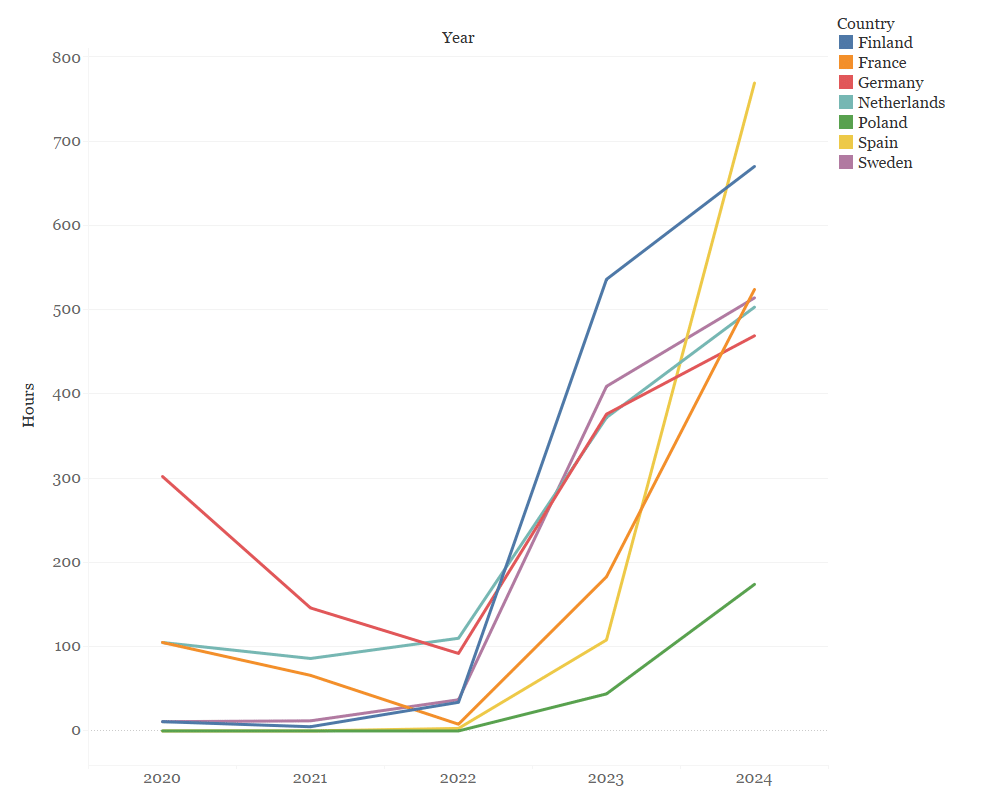

Between 2020 and 2024, the number of zero and negative electricity price events rose sharply across Europe, as shown in Figure 1.

Zero and negative electricity prices across Europe (Source: Ember Hourly Prices; Note: For 2024, data includes events until the end of September).

For instance, Germany had the most occurrences in 2020 (302 hours) but was overtaken by other countries. In Finland, the number of zero or negative prices skyrocketed from just 11 in 2020 to more than 650 in 2024. Spain did not allow negative prices until 2023; however, within just a year, 769 hours of negative pricing were recorded.

Spain and Finland rely heavily on weather-dependent renewable energy sources, leading to similar challenges in their electricity markets. In Spain, abundant solar capacity drives price pressures during sunny days when solar power generation peaks. Similarly, Finland’s substantial wind energy capacity, particularly in coastal regions, causes price dips during periods of strong winds. In both cases, high renewable energy output can saturate the grid when demand is not high enough to absorb the excess supply.

Additionally, both countries are faced with low electricity demand during off-peak hours. Even with flexibility mechanisms in place, it remains difficult to balance supply and demand due to limited incentives for consumers to adjust their energy usage. This lack of demand-side responsiveness exacerbates the issue, leading to a large surplus of renewable energy.

In Germany and France, prices are heavily influenced by high renewable energy generation and low demand during off-peak hours, but at the same time, unique challenges with regulatory issues and grid congestion amplify pressure on prices. As central hubs in Europe’s electricity network, limited interconnection capacity often creates bottlenecks, hindering the export of excess electricity and significantly driving domestic prices downward.

Moreover, renewable support schemes in both countries, such as feed-in tariffs and contracts for differences, incentivise renewable energy generators to produce even during low price periods. While these mechanisms provide financial stability for producers, they can result in excessive generation when combined with low demand, further straining the market balance.

Italy presents an interesting case. While it has so far avoided negative prices due to its unique market structure, the implementation of Integrated Text on Electricity Dispatching – TIDE (Testo Integrato del Dispacciamento Elettrico) in 2025 will allow the country negative pricing, bringing it in line with other European markets. This shift could increase market volatility, particularly in renewable-rich regions like Sicily and Sardinia. TIDE’s introduction highlights the importance of market mechanisms that better reflect real-time supply-demand dynamics.

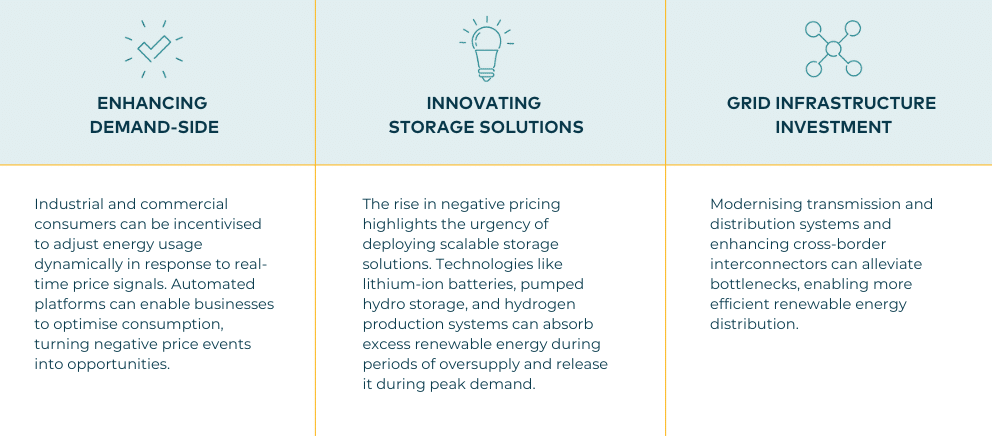

Solutions for addressing negative electricity price events

Effectively managing negative price trends would require a multi-faceted approach. Key strategies could include:

Solutions for addressing negative electricity price trends in Europe could include enhancing demand-side, innovating storage solutions, and ensuring grid infrastructure investment.

Geopolitical factors impacting the European PPA market

Geopolitical factors play a pivotal role in shaping the market and influencing corporate strategies and investment decisions. Recent events, including the outcome of the U.S. elections and the newly appointed European Commission, are expected to impact the European power purchase agreement (PPA) landscape in several key ways.

U.S. elections

A new Trump administration could substantially expand U.S. liquefied natural gas (LNG) exports, thus increasing the global LNG supply and placing downward pressure on European gas. This shift is likely to result in lower gas prices across Europe, subsequently driving down power prices as natural gas-fired plants often set the marginal cost of electricity in many European markets. With reduced power prices, the value of fixed-price renewable energy contracts, such as PPAs, could also decrease.

Increased tariffs on critical green technology components such as solar cells and batteries, a hallmark of anticipated trade policies, are poised to elevate global costs for renewable energy projects significantly. These tariffs, which could exceed 60% for Chinese imports, would disrupt supply chains and inflate the capital expenditure (CAPEX) required for renewable developments, including those in Europe. This could hinder progress in meeting renewable energy goals and make projects less financially feasible.

Reforms by the new European Commission

The newly appointed European Commission is set to significantly influence the European PPA market through the implementation of the electricity market design reforms. The reforms emphasise state-backed guarantees to mitigate credit risks and propose eliminating regulatory barriers to boost renewable energy investments. The Commission also highlighted the strategic role of corporate renewable PPAs in achieving energy transition goals, advocating for standardised methods across member states.

Efforts to enhance grid infrastructure are also underway, with guidelines to prevent disputes over financial responsibilities for large-scale renewable projects and to address grid congestion, ensuring smoother integration of renewables and expansion of the PPA market.

Conclusion

Negative pricing trends and geopolitical uncertainty drive both challenges and opportunities for businesses in the European energy market. To navigate these shifts successfully, market decision-makers must adopt forward-thinking strategies that prioritise flexibility, infrastructure investment, and geopolitical risk management.

Ultimately, by leveraging PPAs as a tool for resilience, businesses can not only mitigate risks but also position themselves to lead Europe’s transition to a sustainable energy future. For a broader perspective on how these dynamics are evolving across global markets, subscribe to receive the upcoming 3Degrees Global Market Report, launching in Q1 2025.

Subscribe to our Global Market Insights Report

Coming soon! Subscribe now to be one of the first to receive it in your inbox.