The Securities and Exchange Commission (SEC) has adopted the long-awaited rule on climate-related financial disclosures. With the global impact of climate change becoming increasingly evident, businesses and their value chains are facing growing impacts. This trend partly explains why 3Degrees has witnessed a rapid increase in corporations and businesses taking meaningful action to address the climate crisis by setting clean energy and other climate-related goals over the past two decades. In fact, a 2023 report showed a 40 percent increase in the number of companies with net zero targets over 16 months, now representing 66% of the annual revenue of the world’s largest 2,000 companies. At the same time, as companies are setting goals, investors are seeking decision-useful information on how a company evaluates and mitigates the risks associated with climate change and how these factors may impact its current and long-term financial performance and position.

|

The SEC points to previous rules and Supreme Court precedent in defining materiality. An impact or risk is considered material if there is a substantial likelihood that a reasonable investor would consider it important when determining investment or voting decisions. Materiality determination is fact specific and based on quantitative and qualitative considerations. As an example, for disclosing GHG emissions, materiality is not solely determined based on the quantity of emissions but rather if a reasonable investor would consider the disclosure of emissions as important in making an investment or voting decisions. |

The SEC’s Enhancement and Standardization of Climate-Related Disclosures for Investors aims to address investors’ needs by adopting rules that require registrants to disclose certain information about climate-related risks that have materially impacted (or are reasonably likely to impact) a company’s business strategy, profit and losses financial statement, or financial condition. Initially announced in early 2022, the proposed rule has undergone notable modifications from its original form after considering approximately 24,000 stakeholder comments over the past few years.

Following a review of the final rule, we will walk you through the key aspects, important details omitted, implementation timeline, and how the rule fits in with other global climate disclosure rules.

The SEC’s “Enhancement and Standardization of Climate-Related Disclosures” Final Rules

3Degrees has highlighted the specific components of the SEC final rule that may impact clients directly, including disclosure of material climate-related risks, details on climate-related targets or goals, the use of carbon credits and renewable energy certificates (RECs), and disclosure requirements for scope 1 and 2 greenhouse gas (GHG) emissions.

Disclosing climate-related risks with a material impact

The final rule creates a new subpart 1500 of Regulation S-K that requires registrants to disclose climate-related risks. It incorporates several modifications from the SEC’s initial rule in response to stakeholder concerns that the requirements were too costly, burdensome, and overly prescriptive. Based on the Task Force on Climate-related Financial Disclosures (TCFD), a well-established framework familiar to many registrants and investors, this approach aims to ease compliance burdens for registrants and help standardize climate-related risk disclosures for investors.

While the SEC adopted similar definitions to those in the the TCFD framework, they did modify the definition of climate-related risks to mean the actual or potential negative impacts of climate-related conditions and events on a registrant’s business, results of operations, or financial condition, including both physical risks and transition risk, that are material. Physical risk is defined as both acute and chronic risks to a registrant’s business. For example, acute risks would include shorter-term severe weather events such as hurricanes, floods, or tornadoes, while chronic risks would include longer-term weather patterns like sea level rise, drought, and extreme temperature changes. Transition risks include increased costs associated with climate-related changes in law or policy, reduced market demand for carbon-intensive products, or competitive pressures associated with the adoption of new technologies.

The SEC does not provide an exhaustive list of physical and transition risks but requires registrants to disclose those that are material. The final rule outlines the temporal standard for how to assess the climate-related risks with material impact by likelihood in the short-term (next 12 months), and separately, in the long-term (beyond the next 12 months).

Disclosing climate-related goals and targets

The SEC’s final rule requires that registrants disclose any climate-related target or goal if those commitments are reasonably likely to materially affect a registrant’s business, operations, or financial condition. This includes any information or explanation to help investors understand the material impact of them, including (as applicable) a description of:

![]()

![]()

The scope of activities included in the target;

![]() Unit of measurement;

Unit of measurement;![]()

![]() Defined timeline by which the target is intended to be achieved, and whether it is based on one or more goals established by a climate-related treaty, law, regulation, policy, or organization;

Defined timeline by which the target is intended to be achieved, and whether it is based on one or more goals established by a climate-related treaty, law, regulation, policy, or organization;![]()

![]() Established baseline for the target or goal, defined baseline time period, and the means by which progress will be tracked; and

Established baseline for the target or goal, defined baseline time period, and the means by which progress will be tracked; and![]()

![]() A qualitative description of how the registrant intends to meet its climate targets or goals.

A qualitative description of how the registrant intends to meet its climate targets or goals.

![]()

In the final rule, the SEC made several modifications to the proposed rule to ensure it was not overly prescriptive or burdensome. To that end, the items listed above are non-exclusive examples of the additional information that registrants must disclose if it is necessary to understand the material impact of the target or goal.

RECs and Carbon Credits

In addition to disclosing climate-related goals or targets, registrants must also disclose information related to the use of carbon credits or renewable energy certificates (RECs), if either is used as a material component of a registrant’s plan to achieve those targets or goals. It specifically requires the aggregate amounts of:

- Carbon credits and RECs purchased;

- Capitalized costs associated with carbon credits and RECs; and

- Losses incurred on the capitalized carbon credits and RECs during the fiscal year.

If material registrants would also be required to disclose the following:

![]()

![]() The amount of carbon avoidance, reduction, or removal represented by the credits or the amount of generated renewable energy represented by the RECs;

The amount of carbon avoidance, reduction, or removal represented by the credits or the amount of generated renewable energy represented by the RECs;

![]()

![]()

The nature and source of the credits or RECs;

![]()

![]()

A description and location of the underlying projects;

![]()

![]() Any registries or other authentication of the credits or RECs; and the cost of the credits or RECs

Any registries or other authentication of the credits or RECs; and the cost of the credits or RECs![]()

GHG emissions disclosure requirements

Unlike the proposed rule, the final version requires only registrants classified as large accelerated filers (LAF) or accelerated filers (AF) to disclose their scope 1 and/or scope 2 GHG emissions on a phased-in basis, if such emissions are material.The final rule exempts “smaller reporting companies” (SRCs) and “emerging growth companies” (EGCs) from reporting these emissions. There are a number of qualifications that define an SRC and an EGC, which can be found in the footnotes on Page 17 of the final rule.

When material, registrants will be required to disclose any described scope of emissions in the aggregate in terms of carbon dioxide equivalent (CO2e), which is the amount of metric tons of CO2 emissions that have the same global warming potential as one metric ton of another greenhouse gas. If any constituent gas in the disclosed emissions, such as methane, is individually material,, andthen it must also be disclosed disaggregated from other gasses.

The final rule requires registrants to describe the methodology, significant inputs, and significant assumptions used to calculate their disclosed GHG emissions. However, as with other parts of the final rule, this disclosure is less prescriptive than it was in the proposal, aiming to provide greater flexibility and present the information in a manner that best fits with their particular circumstances. The proposed rule would have required registrants to use the same scope of entities and other assets in its consolidated financial statements when determining the organizational boundaries for its GHG emissions disclosure. The final rule allows for different organizational boundaries; registrants must only provide a brief explanation of this difference in sufficient detail for a reasonable investor to understand.

Additional aspects of the final rule include requiring an attestation report for registrants disclosing their scope 1 and/or scope 2 GHG emissions and safe harbor provisions for forward-looking statements in connection with certain disclosures, such as goals and targets.

Disclosure of scope 3 emissions not required by SEC’s final climate rule

Most notably, the final rule eliminates the requirement to disclose scope 3 emissions for all registrants. The SEC cited concerns over the potential burden this requirement could impose on some companies, as well as uncertainty regarding the robustness, reliability, and accuracy of data required for scope 3 emission calculations.

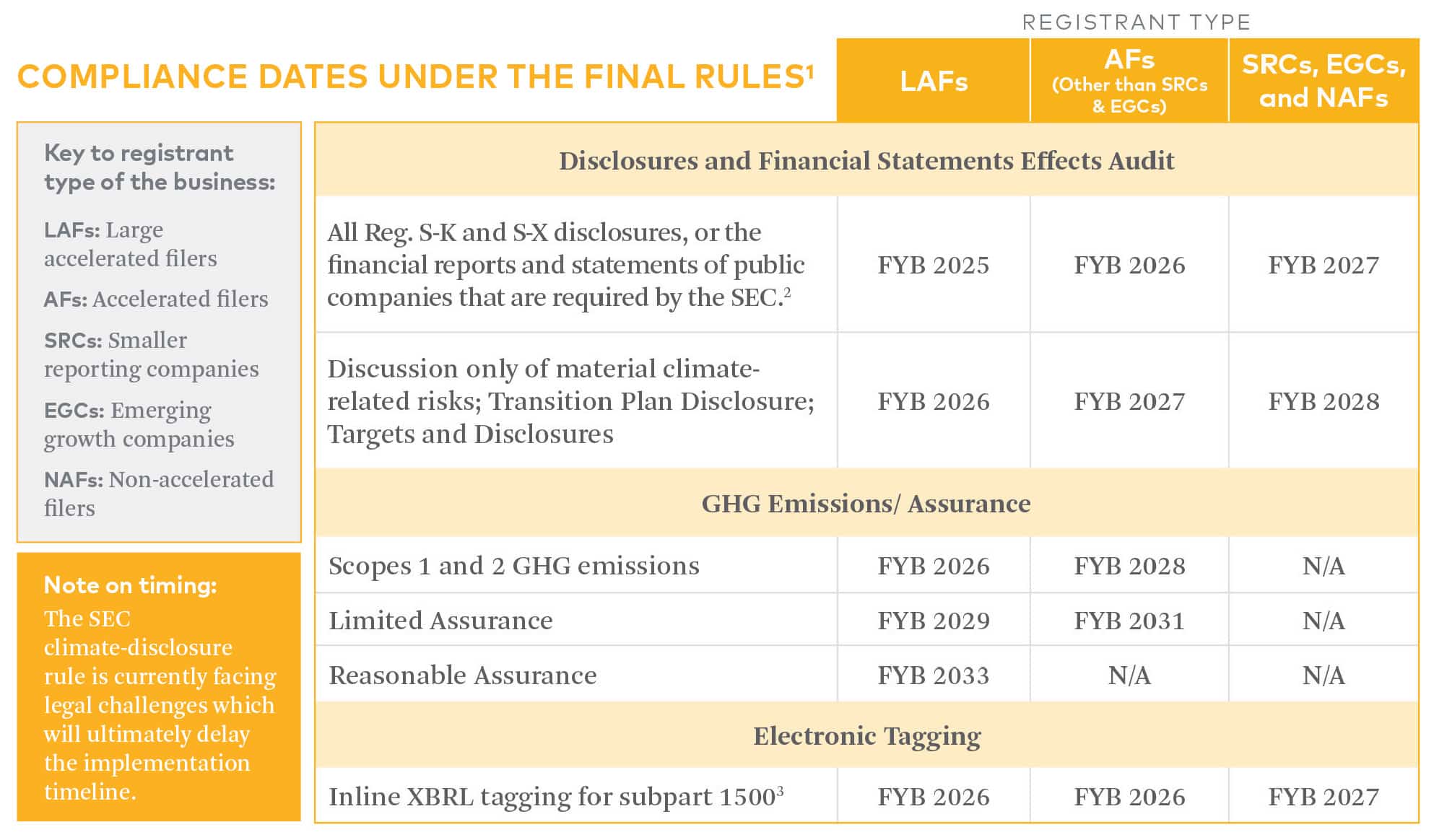

Timing for the final SEC climate-related disclosure rule to go into effect

The final rules will become effective 60 days after they are published in the Federal Register. Once effective, the rule will be phased in according to the registrant type of the business – LAFs, AFs, SRCs, EGCs, and non-accelerated filers (NAFs).

The timing also provides several accommodations, such as:

- Additional phase-in periods for disclosures related to material spending, GHG emissions and assurances, and electronic tagging

- Safe harbor from private liability for climate-related disclosures

- Exempting SRCs and EGCs from the GHG emissions disclosure requirement

- Allowing scope 1 and/or scope 2 emissions disclosure to be filed on a delayed basis with specific guidelines for domestic registrants, foreign private issuers, and those filing a Securities Act of Exchange Act registration statement

A view of how the SEC climate-related disclosure rule will be phased in.

Interoperability with other climate-disclosure rules in CA, EU, and ISSB

The SEC’s final climate-related disclosure rule enters a crowded field of other climate-related disclosure frameworks and regulations, such as the International Sustainability Standards Board (ISSB)’s climate-related disclosures (IFRS S2), California’s Climate Corporate Data Accountability Act (SB-253) and Climate-Related Financial Risk Act (SB-261), Corporate Sustainability Reporting Directive (CSRD) in Europe, and more. These regulations all incorporate recommendations similar to that of the TCFD framework. For registrants preparing to comply with other regulations, the burden of adhering to the SEC final rule may be minimal. Despite being a watered-down version of TCFD to reduce costs for registrants, the SEC’s final rule is still intended to work with other climate-related financial disclosures. Each of the rules has similar requirements, which can make filing for each easier.

As can be seen from these laws and regulations – along with the many jurisdictions that are considering adopting the ISSB standards, like Australia, Canada, Hong Kong, the United Kingdom, and more – the importance of climate-related disclosures and corporate compliance is rapidly increasing. 3Degrees supports the disclosure of consistent, comparable, and reliable information to help businesses and investors better assess climate-related risks.

In future content, we’ll be investigating how these climate-related financial disclosures relate to one another, so sign up for our newsletter for updates. If you need any assistance navigating this new climate guidance, please contact us.