Almost 2.5 years after the Science-based Targets Initiative (SBTi) first introduced the concept of “Beyond Value Chain Mitigation” in its Corporate Net-Zero Standard, this week the prominent climate standards organization released its detailed Beyond Value Chain Mitigation guidance, totaling nearly 200 pages.

To contribute to “Beyond Value Chain Mitigation” (BVCM), companies support efforts to reduce emissions that do not sit within their value chains. Companies might choose to do so in recognition of risks that greater climate change may soon pose to their businesses, to attract and retain sustainability-minded customers, employees, and investors, to leverage tax incentives, or even to shore up certain parts of their supply chains, such as farms and forests. Historically, the purchase and retirement of carbon credits has been the default way companies have carried out BVCM, then measured and reported the impacts of their efforts. But given the urgency of ratcheting up mitigation ambition on all fronts, as well as scrutiny and criticisms of carbon credit use in recent years, a clear need has emerged for further guidance on how companies can effectively and transparently advance mitigation beyond their own footprints.

The new SBTi BVCM guidance outlines processes companies can apply to effectively design and implement high-integrity and high-impact BVCM strategies. It then provides supporting detail in the form of case studies and a proposed “toolbox” for diverse actors (e.g., policymakers, investors, customers) to help lower outstanding barriers to greater BVCM action. Overall, the new guidance provides a much-needed positive endorsement for corporate use of high-quality voluntary carbon credits as one component of a credible climate mitigation strategy.

How should I use this guidance if my company has an SBTi target (or will have one soon)?

To align with SBTi guidance, companies can leverage the new BVCM reports to act upon SBTi’s recommendation (optional, but encouraged within the Net-Zero standard) that companies “should take action or make investments outside their value chains to mitigate GHG emissions.” SBTi has noted it does not plan to validate BVCM claims, particularly given that other initiatives are already working to define high-quality BVCM-related claims, such as the Voluntary Carbon Market Integrity Initiative (VCMI). More broadly, companies with SBTi targets can use this guidance to build a business case for further climate action beyond their value chains, including the use of high-quality carbon credits, backed by one of the most prominent voluntary climate standards organizations in the world.

How should I use this guidance if my company does not have an SBTi target?

Companies choosing not to engage with the SBTi target-setting guidance and validation process but still striving to mitigate emissions can also look to this guidance for help developing effective BVCM strategies or more specific carbon credit strategies. They can also leverage this guidance, particularly drawing upon SBTi’s credibility and backing of high-integrity carbon credit use, to help build a strong case for the use of quality carbon credits as part of an effective climate strategy. However, the BVCM guidance clarifies that all companies should get their own house in order (i.e., set, plan to implement, and begin pursuing their own scope 1, 2, and 3 emission reduction targets) before turning their attention to any mitigation beyond their footprints, such as carbon credit procurement.

What does the new guidance say about taking action on BVCM?

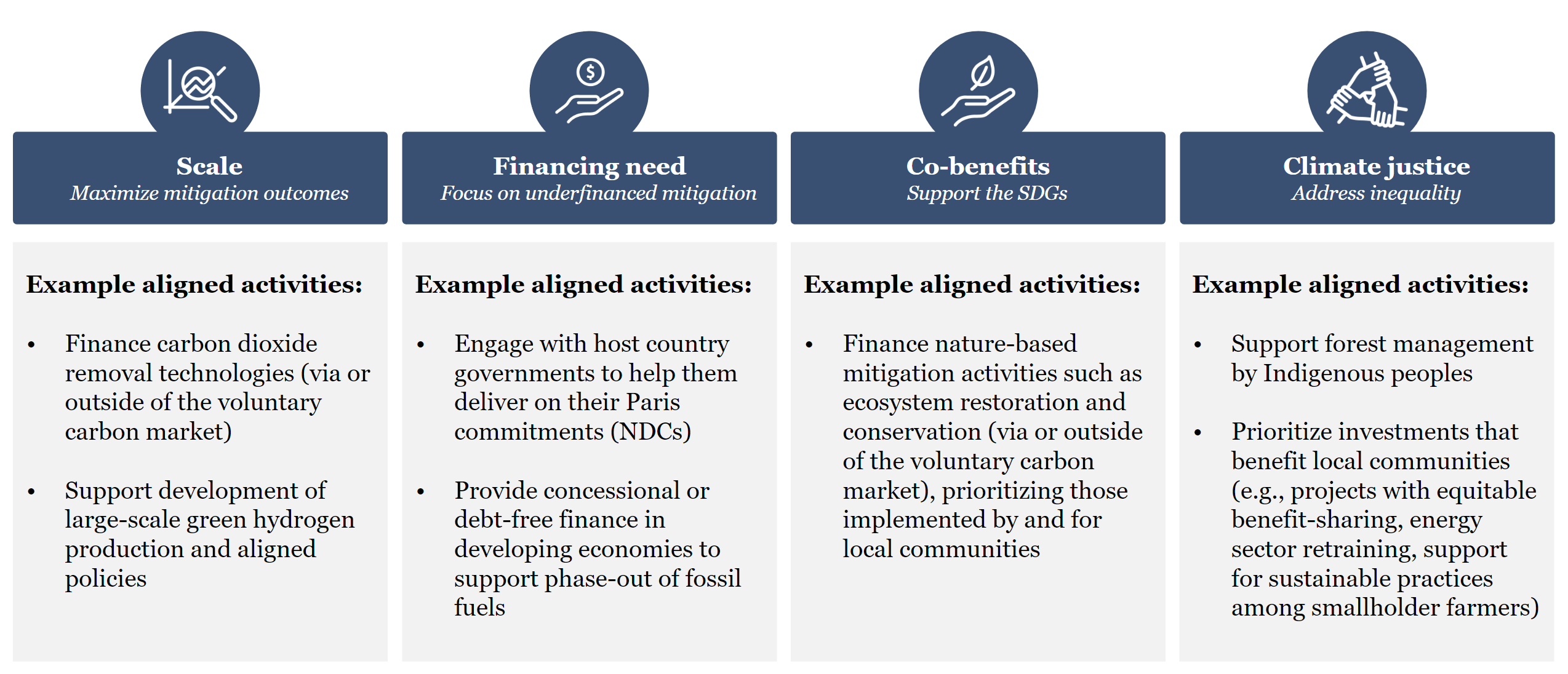

For companies ready to establish a BVCM pledge, SBTi lays out two goals to inform overarching BVCM strategies, as well as four principles to guide more detailed design of portfolios of BVCM activities.

Goals to inform BVCM strategy

Principles to inform BVCM portfolio design

As is clear from this sample list of activities, SBTi’s definition of BVCM is flexible enough to encompass many different mitigation aims and ways of achieving them. While several provided examples of high-quality BVCM goals implicitly or explicitly promote carbon credit use, several other, non-carbon credit examples of effective BVCM actions are included as well.

In addition, SBTi does not lay out any specific requirements for tracking the impacts of this wide range of non-carbon-credit based BVCM activities the guidance allows. While the guidance does explicitly call for annual disclosure of BVCM investment amounts and third-party verification of claimed outcomes, it leaves additional specific approaches to measurement, reporting, and verification largely up to the reporting company.

In contrast to its flexible treatment of BVCM activity and measurement options, SBTi does include a more prescriptive definition of best practices when it comes to setting a BVCM budget and then allocating part of this budget towards carbon credits.

How much budget should my company allocate to BVCM?

While drafting this guidance, SBTi sought feedback on how best to estimate the “right” amount of resources companies should allocate to BVCM. Should companies set aside funds in proportion to their profits or revenues (money-for-money), in proportion to estimated costs of intervention efforts needed to neutralize their unabated emissions (ton-for-ton), or in a pre-set proportion (using a consistent cost of carbon as a multiplier) to their unabated emissions (money-for-ton)?

In the final guidance, SBTi lays out all of the above options as methods companies can use to determine the scale of their BVCM pledge, recognizing companies have different abilities and willingness to pay for BVCM, and provides fictionalized case studies of companies using each one of these options. Across the four illustrative examples provided, regardless of the selected allocation approach, each company pledges between 1% and 2% of annual profits for its BVCM activities of choice.

SBTi also specifies one allocation option as “best practice” for defining the scale of BVCM pledges: the “money-for-ton” approach, using an internally agreed carbon price. Specifically, SBTi recommends that companies “apply a science-based carbon price to unabated scope 1, 2, and 3 emissions” to determine a BVCM budget, then use a portion of this calculated budget to purchase high-quality carbon credits matching at least 50% of unabated emissions each year.

Are any kinds of BVCM claims or investments not allowed by SBTi?

Surprisingly few types of claims and investments have been carved out by SBTi as illegitimate ways of pursuing BVCM. Approaches the guidance does discourage include:

- Low-integrity claims, as defined by Voluntary Carbon Markets Integrity Initiative (VCMI) Principles for Climate Mitigation Claims Credibility (i.e., claims that are misleading, inaccurate, or not traceable / verifiable)

- Use of carbon credits with vintages older than 2021 (i.e., that represent mitigation outcomes that occurred before 2021), in pursuit of the near-term mitigation goal

- Use of low-quality carbon credits, as defined by prominent standards and guidelines in the market (the guidance references the Integrity Council for Voluntary Carbon Markets’s Core Carbon Principles, the Tropical Forest Credit Integrity guide, and the Carbon Credit Quality Initiative as recommended resources to identify high-quality credits).

In addition, while the guidance cautions against compensation (i.e., offsetting or neutralization) claims based on BVCM activities, noting they have been “increasingly the subject of public scrutiny and regulation,” it does not rule these out as legitimate BVCM claims.

What’s next for companies with SBTi targets or carbon credit procurement plans looking to align with this new guidance?

First, companies with SBTi targets already purchasing carbon credits can now rest assured that carbon credits (including avoidance credits) can play a credible role, as defined by robust guidance, within a science-aligned climate strategy. Further, companies with or without SBTi targets interested in making compensation-based claims (e.g., claiming that emissions from a given product / service have been “neutralized” or “offset” by carbon credits, perhaps to help make an internal business case for procurement), can leverage SBTi’s guidance on how to set a high-impact BVCM strategy that encompasses such volumetric matching claims while still maintaining transparency and integrity. Lastly, all companies (with or without SBTi targets) can leverage SBTi’s endorsement of using high-quality carbon credits as one part of an effective climate strategy to help build their business case for further investment in the voluntary carbon market.

If you are considering investing in carbon credits or other beyond value chain mitigation actions, making associated claims, shifting your existing carbon strategy to consider impact and contribution more broadly, or have any questions about what evolutions in guidance mean for your existing or forthcoming climate commitments, please reach out.

Tory Hoffmeister is a Manager on 3Degrees’ Energy and Climate Practice consulting team

Elizabeth Geller is a Director on 3Degrees’ Energy and Climate Practice consulting team