Power Purchase Agreements (PPAs)

Advance your renewable energy commitments with a PPA

Power purchase agreements (PPAs) can be a great option for organizations who want to make significant progress toward achieving their renewable energy targets. 3Degrees’ trusted, proven corporate PPA transaction expertise enables us to provide end-to-end support for sourcing PPAs, including stakeholder education and alignment, procurement strategy, RFP management, PPA negotiations, and post-execution PPA monitoring. We can manage the entire process on your behalf – or assist with tactical steps in the process.

What is a PPA?

A PPA is a contract between a buyer and a seller, typically a corporation and a renewable energy developer, in which the buyer purchases the electricity and energy attribute certificates (EACs) from a specific renewable energy project. PPAs are a good mechanism for companies to make a long-term commitment to procuring renewable energy. They can be structured as a physical PPA, where the energy and EACs are physically delivered to the buyer, or a virtual PPA in which the contract is financially settled and the EACs* are delivered to the buyer.

Why consider a PPA?

- No capital investment

- Potential for positive NPV

- May act as a hedge against competitive retail prices

- New projects create clear, positive environmental impact

- Single transaction can make a meaningful contribution for goals

- No changes required to operational power procurement and management

Want to complement your PPA strategy?

Learn how transferable tax credits (TTCs) can deliver near-term tax savings while helping bring new projects online.

PPA transaction services

The 3Degrees team has global expertise in all aspects of evaluating and implementing renewable energy transactions. Each client engagement is broken out into three distinct phases.

- Comprehensive electricity usage analysis

- Educational workshops

- Procurement strategy

- PPA business case

- Go/No Go decision on procurement

- Design, issue, and manage RFP

- Proposal evaluation and due diligence

- Shortlisting, interviews, and award

- Go/No Go decision to award and negotiate

- PPA contract negotiations and execution

- PPA responsibilities checklist

- Monitor development milestones

- PPA performance monitoring

- Invoice auditing

- EAC transfers and retirement

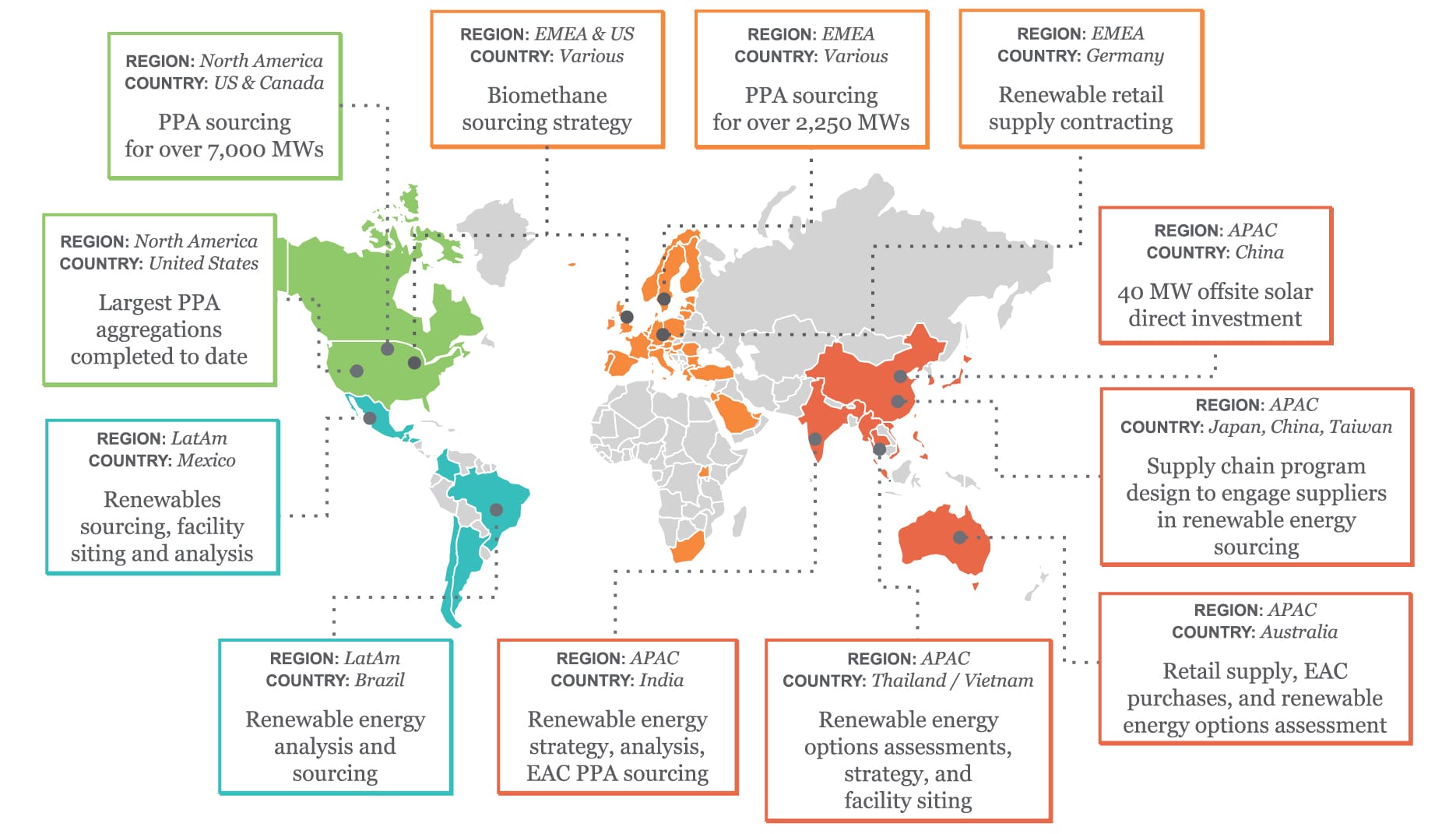

Global, trusted renewable energy advisor

Our team has navigated the complexities of renewable energy markets worldwide. We’d love to partner with you to help bring your next project to life.

renewable energy transactions executed

GW PPA transactions executed

countries supported through renewable energy consulting

Explore featured projects

of

As part of their journey to reach a 2050 goal of net zero greenhouse gas emissions, Mondelēz International has been working towards its aim to reduce its scope 2 footprint worldwide. 3Degrees worked with the global snacking company to educate and align stakeholders on the current state of European energy markets and PPAs, determine the best-fit project characteristics to meet the company’s needs and preferences, and ultimately sign a 12-year PPA with a renewable energy developer in Poland for approximately 126 GWh of solar electricity.

By joining together, smaller energy users can create enough buying power to make a material impact on a project’s financial outlook, attracting the attention of project developers and opening this impactful solution to a wider range of companies. Akamai, Etsy, and Swiss Re collaborated with larger energy buyer Apple as they leveraged their collective buying power in one of the largest corporate renewable energy transaction to date. This aggregation resulted in six PPAs – the largest one greater than 130 MW and the smallest less than 5 MW.

The climate action journey is long and numerous companies have already taken steps to address their scope 2 electricity emissions. While that’s a great start, most organizations’ scope 3 – or indirect emissions – make up more than 90% of their total GHG emissions inventory. If your supply chain emissions are significant, a supplier PPA aggregation could be an ideal scope 3 reduction pathway to pursue. This article covers benefits, possible structures, and other components of a successful supplier PPA aggregation.

Other renewable energy advisory services

- Detailed investigation of available renewable energy options in any country

- Evaluate viable options based on your current and anticipated consumption profile and organizational priorities

- Receive custom implementation roadmap aligned with your goals and timelines

- Source EACs from new renewable energy projects without a long-term PPA

- Understand project-specific attributes and contract around development risks

- Leverage 3Degrees’ EAC trading desk to optimize your renewable energy portfolio

- Assess scope 2 electricity emissions from your supply chain

- Identify opportunities for supplier renewable energy aggregation

- Support aggregation from strategy to contract execution

- Regulatory analysis to understand H2 requirements & incentives

- Electrolyzer siting analysis to optimize renewable energy supply

- Execute PPA procurement to secure renewable energy supply

The signing of this VPPA is a major advancement towards achieving our aggressive global emissions reduction goals. We are thrilled about this partnership with Enel Green Power North America to help bring new renewable generation online, and appreciate 3Degrees’ strategic guidance and implementation support that helped make this transaction possible.”