In an effort to increase the quantity of clean hydrogen (H2) in the U.S., the Inflation Reduction Act (IRA) incorporated a 10-year production tax credit based on the carbon intensity (CI) of the H2 produced, often referred to as the 45V tax credit. The Treasury Department recently released additional guidance on CI accounting, including through the use of book-and-claim accounting of renewable energy certificates (RECs).

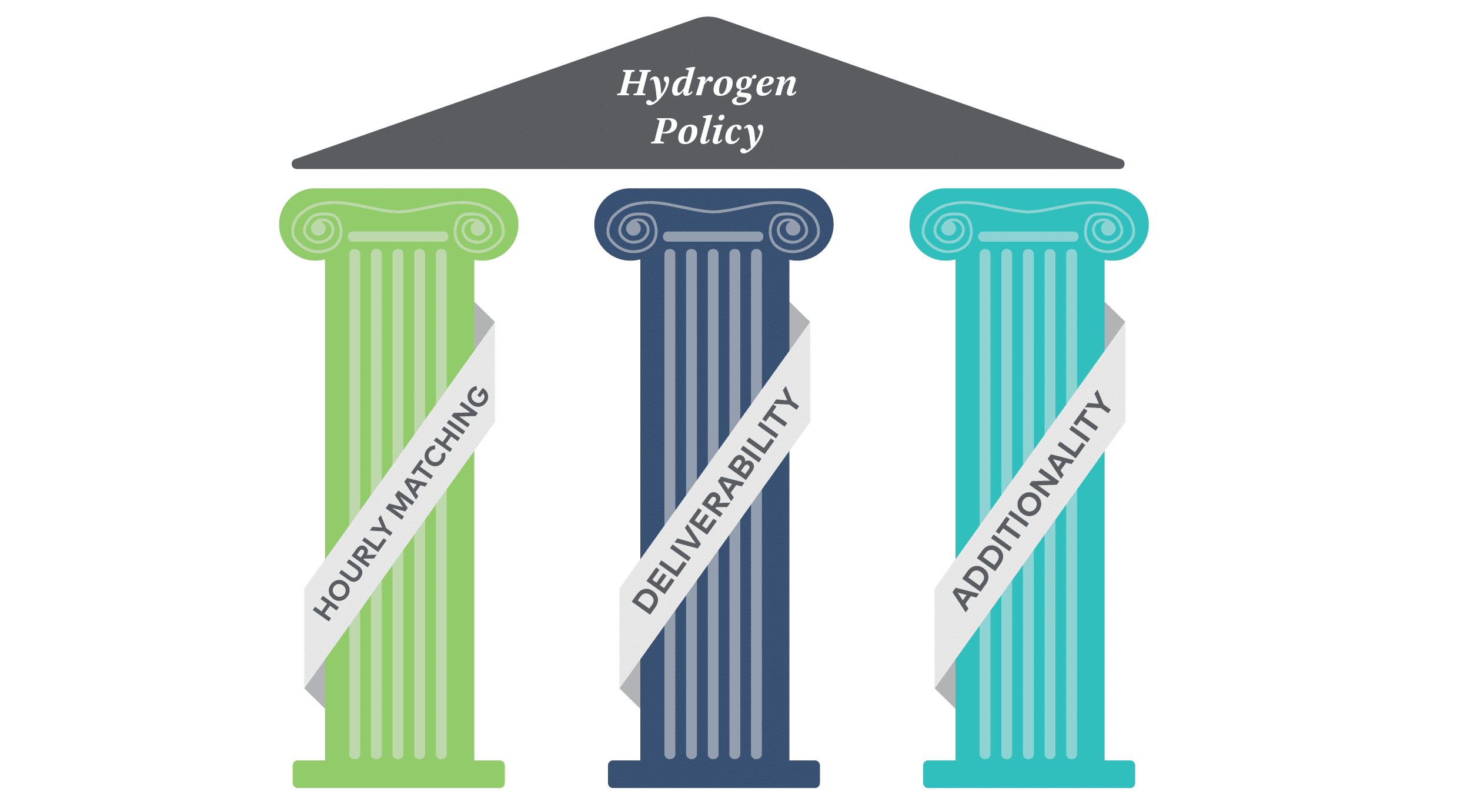

This guidance enables organizations to match energy used in the production of hydrogen via electrolysis with qualifying unbundled RECs, effectively lowering the CI score of the hydrogen product. The guidance applies the widely accepted three-pillar approach to emissions reductions of hourly matching, deliverability, and additionality requirements by specifying that RECs meet certain geographic and temporal criteria. While the final 45V guidance will likely put upward pressure on several regional REC markets in the medium- to long-term, the extent of the impact on prices is uncertain.

However, we can discern 45V’s current market impacts, along with what impact it may have on corporate buyers. Read on for our overview of the 45V guidance.

Stay informed on hydrogen

Get the latest version and subscribe to future editions of 3Degrees’ Transportation Markets Report to keep track of regulatory updates that impact hydrogen.

REC qualification requirements

Under the proposed rule, RECs that meet the following criteria can be matched to qualifying electrolytic H2 production to substantiate a lower CI:

Generation must come from renewable energy facilities with a commercial operations date (COD) within three years of the hydrogen facility’s placed in service (PIS) date. Incremental generation from capacity upgrades (uprate) also qualifies. For example, if the hydrogen facility is placed into service in October 2025, the renewable energy facility must have a COD of November 2022 or later.

Power must be sourced from the same region as the hydrogen producer, as identified in the map on page 3 of the DOE’s 2023 National Transmission Needs Study.

Annual matching is allowed until 2028. Hourly matching will be required thereafter. This means that RECs generated in 2026 can be matched with electricity used in hydrogen production in 2026.

Green-e® or other certification of RECs is not required, however, Center for Resource Solutions (CRS) is in the process of developing a clean hydrogen standard aligned with 45V tax credit criteria. RECs must be verified by a third-party auditor to ensure criteria are met, and are properly registered and retired in a qualified tracking system1.

Clean hydrogen project eligibility

Specific requirements apply to both the facility and the taxpayer to qualify for the investment tax credit (ITC).

Qualified Hydrogen Facility

To receive the 45V credit, the hydrogen facility must begin construction before 2033. The facility cannot also claim the 45Q carbon capture and sequestration credit provided under the IRA.

The H2 produced must be primarily for sale or use; that is, if the hydrogen is flared, vented, or used to produce more H2, or if the cost to produce the H2 is less than the credit, the credit will be reduced or not awarded. Hydrogen may be stored before its sale or use without changing its eligibility for 45V.

Taxpayer

The taxpayer eligible for the credit is the owner of the qualified H2 production facility at the time of the qualifying hydrogen’s production.

ITC Conversion

The default structure of the 45V tax credit is as a production tax credit (PTC). However, H2 producers may elect to claim an investment tax credit (ITC) in the PIS year for the facility. The amount of the ITC would be based on the facility’s expected CI score. If the facility has been designed to minimize the hydrogen’s CI score, the entity can claim the maximum credit. However, the ITC is subject to recapture, so the entity must file an annual report verifying the average CI score of hydrogen produced for each five years after PIS.

REC market impacts

The 45V guidance is likely to increase the demand for RECs across the U.S., especially in regions with existing or emerging H2 production facilities, such as Texas and the Midwest.2 It’s not yet clear how this new demand will interact with Green-e® supply, however, there are some mitigating factors on this market’s development:

- Demand for green hydrogen in the U.S. is driven primarily by consumer choice, unlike in Europe where there are mandates and production targets. This means that unless and until green hydrogen is truly cost competitive (at this point would essentially require maxing out the 45V credit, which ranges from $0.60-$3.00 per kilogram of H2), there is somewhat of an economic barrier to the development of new electrolytic facilities.

- The Treasury’s approach to the three-pillars—hourly matching, deliverability, and additionality— is more restrictive than some of its European regulatory counterparts. The hydrogen industry has concerns about the ability to procure compliant RECs at a reasonable price, especially for smaller producers with less overall funding that are often unable to to afford to co-locate electricity production and will need to rely on grid energy for operations.

- Many investors are waiting for the rules to be finalized before making long-term investments. Similarly, hydrogen consumers are awaiting certainty before agreeing to long-term contracts.

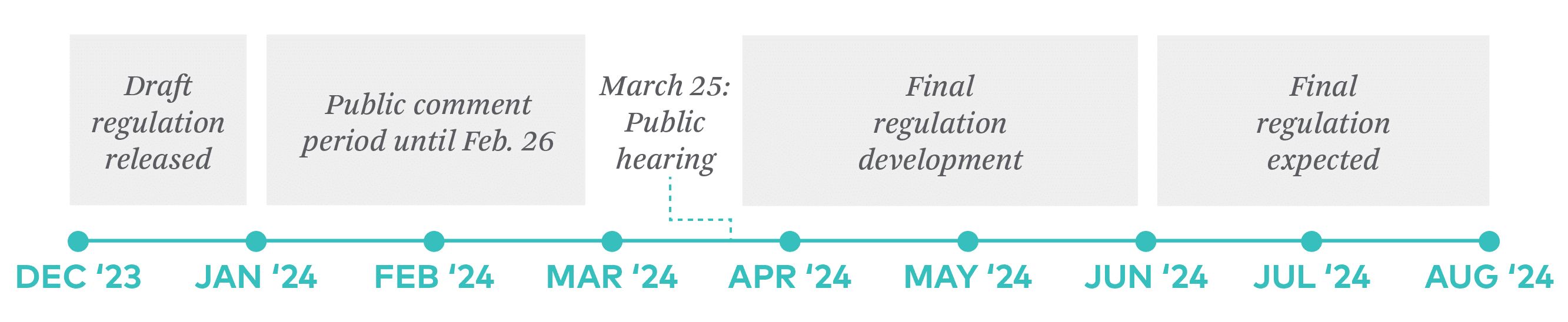

45V tax credit guidance status and timeline

The draft regulation was released by the Treasury Department in December 2023 and the public comment period for the proposed regulation runs through February 26, 2024, which will be followed by a public hearing in March. The relevant federal agencies will then work to review the feedback received and make changes to the draft regulation.

The final regulation is expected in June or July—any later and it will become subject to review by the new administration post-election.

While there is still a lot to be determined prior to the final regulation being announced, we’ll be keeping a close eye on the 45V guidance’s impact on the market. If you’d like to discuss what this means for your organization in more detail, please reach out.

- Qualified EAC registries currently include, but are not limited to, the following: Electric Reliability Council of Texas (ERCOT); Michigan Renewable Energy Certification System (MIRECS); Midwest Renewable Energy Tracking System, Inc. (M-RETS); North American Registry (NAR); New England Power Pool Generation Information System (NEPOOL-GIS); New York Generation Attribute Tracking System (NYGATS); North Carolina Renewable Energy Tracking System (NC-RETS); PJM Generation Attribute Tracking System (PJM-GATS); and Western Electric Coordinating Council (WREGIS).

- https://www.canarymedia.com/articles/hydrogen/new-clean-hydrogen-rules-will-favor-some-regions-more-than-others