Under the Corporate Sustainability Reporting Directive (CSRD), about 12,000 EU companies are obligated to disclose non-financial information relating to their 2024 performance. This will increase over the next few years towards 50,000 companies both within and outside of the EU. The CSRD establishes the European Sustainability Reporting Standards (ESRS), which cover a wide range of ESG topics, and naturally, some will be more relevant to an organisation, its stakeholders and investors than others.

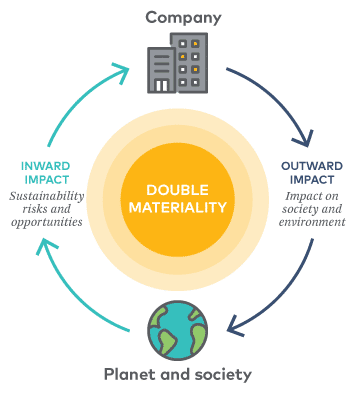

To accomplish the first step of compliance and focus their efforts, companies must determine the scope of their disclosures by performing a double materiality assessment (DMA). The DMA is an essential, required component of the CSRD designed to intentionally direct companies to go beyond their financial performance and internal operations, and understand the greater impacts, risks and opportunities (IROs) of society and the environment on the company, and vice versa.

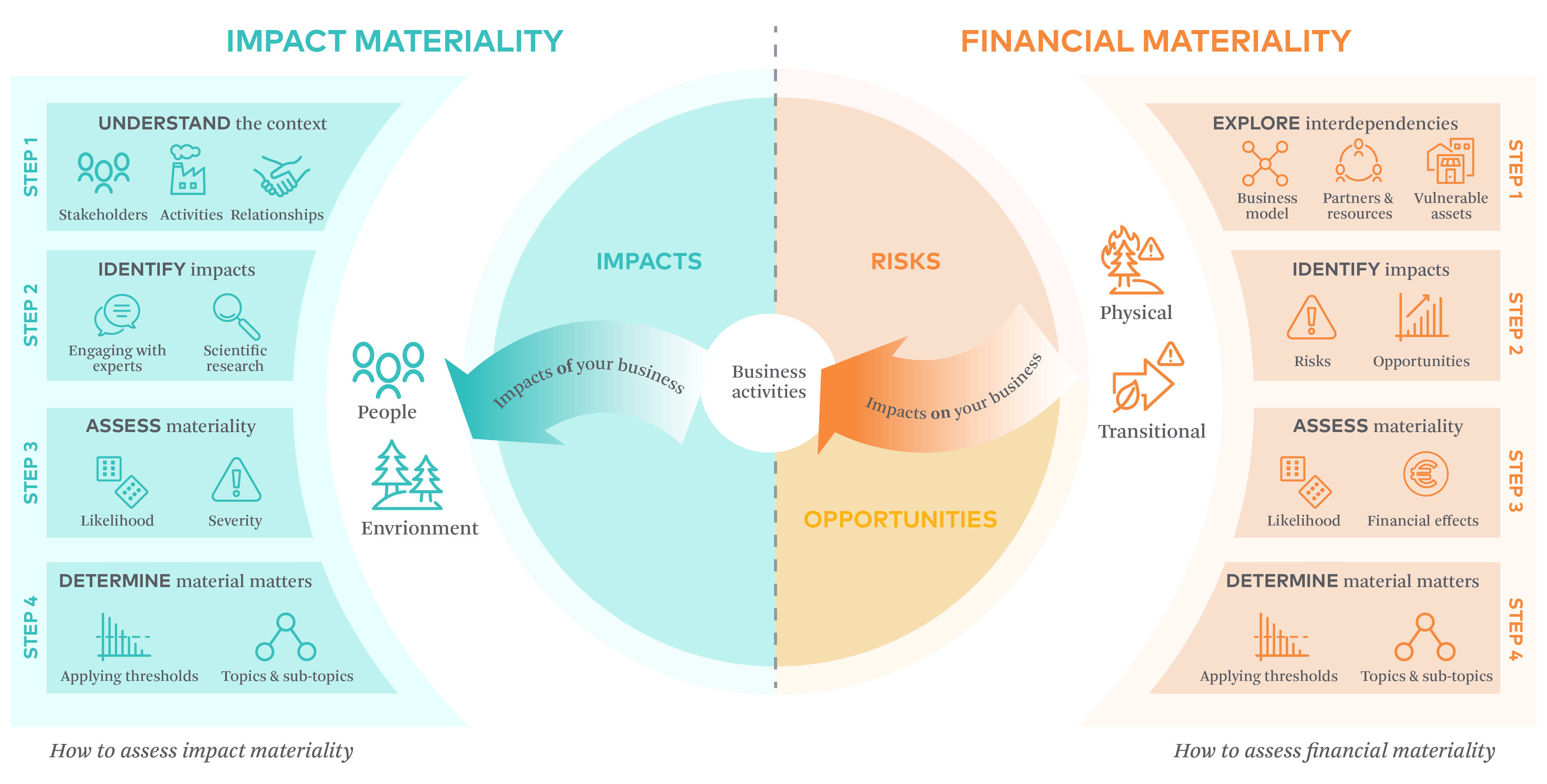

The CSRD differs from other sustainability regulations in its approach to materiality. The ESRS consists of 10 topical standards, containing over 80 potential disclosures and many hundreds of data points, therefore it is essential for an organisation to perform a DMA to know where to focus their collection and inquiry. CSRD requires a more comprehensive approach to materiality assessment than what is currently common practice, and companies will need to extend, evolve and strengthen their existing processes. This is a key first step in any company’s preparations for CSRD disclosure.

To set your organisation up for success, we will walk you through best practices for the DMA and stakeholder engagement required for robust CSRD compliance.

What is new in the double materiality assessment?

Companies often have some experience in measuring and reporting aspects of their “impact materiality” – the effect of the company on society and the environment in which it operates – which may determine ESG priorities such as health and safety goals and greenhouse gas emissions reductions. However, CSRD and the ESRS require a more in-depth evaluation, including:

- Broader coverage of ESG topics, including potentially unfamiliar topics such as biodiversity and ecosystems

- Consideration of “financial materiality” – how these topics do (or may in the future) financially impact its business (note that together, impact materiality and financial materiality make up double materiality)

- Consideration of the full value chain, from raw materials to end use and disposal

- Consideration of both positive and negative, current and potential IROs.

When it comes to the DMA, impact materiality will often be an organisation’s starting point, followed by analysis of financially material topics. Examples of impact materiality are pollution, or the use of hazardous materials, and an example of financial materiality is disruption to the supply chain due to increased droughts or flooding.

When a company undergoes a DMA, they explore interdependencies within the business model and value chain to reveal areas of opportunity. There might be an opportunity to develop resilience to predicted adverse effects or take advantage of evolving their business activity / model. The DMA approach promotes broader awareness, as each company is urged to look at itself within a wider context, one where it isn’t only the subject impacting society and environment but an object that is being impacted as well.

Performing the DMA allows the users of the disclosures – investors, lenders, insurances, and customers – to provide decision-useful information to the board and relevant teams within the company.

Key steps for an effective DMA

Conducting a successful DMA requires a targeted, robust data collection and management system. Complex and wide reaching, the DMA will require significant planning and organisation. We suggest creating a designated cross-department team (including representation from sustainability, risk, and finance) responsible for this task.

- When performing a DMA, it is imperative to define boundaries and key terms, such as time horizons. The team should map out the business operations and value chain in as much detail as possible. For best results, it is critical to set out clear definitions and outline the scope under which the DMA is carried out. Once this foundation has been established, it’s time to identify potential material topics and IROs.

- By creating a preliminary list of topics, impacts, risks and opportunities that might be material to the organisation, a targeted stakeholder engagement program can be designed. First, an organisation should explore the relevance of each of the ESRS topics on its business operations and value chain. Using existing science, reports, previous materiality assessments, desktop research, light touch internal conversations, and standards, the team can identify potential material IROs for further investigation.

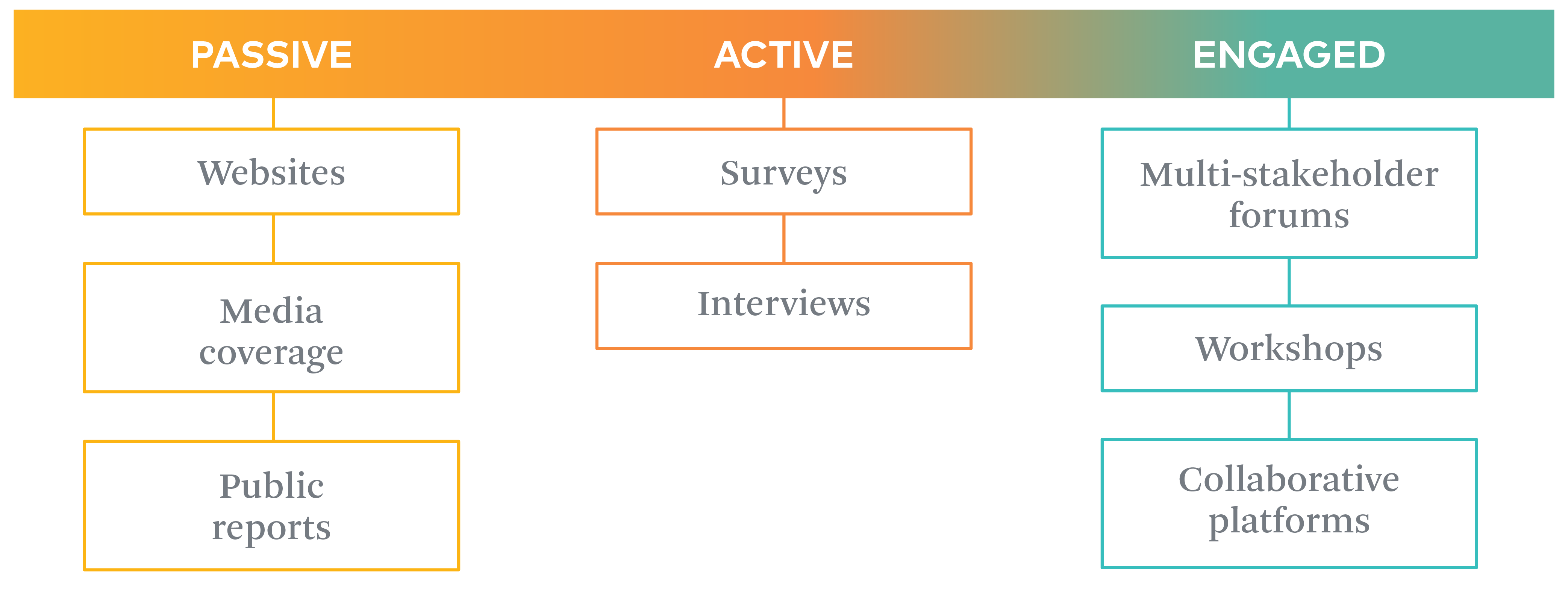

- Stakeholder engagement takes many forms, and there are a lot of tools and sources at a company’s disposal. The optimal approach should aim to strike a balance between collecting meaningful insights and limiting administrative burden for all parties. However, it is worth noting that this phase is likely to change over time as the company’s process matures and the disclosures evolve. Engaging relevant stakeholders to gather the necessary insights on potentially material matters is an extensive process, and a hugely important step in the overall assessment. We will expand more on this in the following section.

- Once stakeholder feedback and insights have been collected it is time to score the IROs and apply carefully developed materiality thresholds to determine what is material. This filtration process allows the team to confirm material IROs, as well as confirm the material sustainability topics and which details to disclose on.

- The last key step is to engage senior leadership to obtain sign off on the material sustainability matters and share the outcome of the DMA as appropriate.

Focus on stakeholder engagement

When beginning to engage stakeholders, a team should map out who should be consulted and identify the preliminary work that needs to be done prior to engagement. The ESRS recognises two key categories of stakeholders: those that are (or will be) impacted — such as customers, suppliers, and local communities — and users of the sustainability statements, such as investors and industry groups. The ESRS also recognises the existence of stakeholders who cannot voice their concerns, one example being the natural world.

The process of stakeholder engagement first involves the identification of stakeholders with the right insight and the assignment of applicable topics to each stakeholder. The choice of stakeholders selected will depend on the company’s unique context, its business activity, the structure of its value chain, and the preliminary list of potential material topics.

Tailoring engagement questions and styles to particular stakeholders will yield the most valuable responses. It’s useful to consider the intended level of contribution that can be expected from each stakeholder ahead of the consultation, and to design the engagement accordingly, for example using written questionnaires, interviews, and workshops.

Questions should be tailored to be relevant to each stakeholder and should take into account:

- How they are impacted by a particular topic or IRO

- If they are in a position to provide insight on a particular topic or IRO

- What is their position in the value chain

Next, the team should extend an invitation to stakeholders to participate in the DMA. The way this is carried out is crucial, and incentivising stakeholder participation can help ensure success.  The final step in the stakeholder engagement process is to review the responses and apply learnings. Stakeholder feedback is a valuable resource that can be used to validate the identified list of potentially material topics and inform the scoring and materiality assessment of identified impacts. It also can inform the list of potentially material risks and opportunities relating to resource use and business relationships. Stakeholder responses may raise additional questions, and in some cases, it may be appropriate to follow up for more information.

The final step in the stakeholder engagement process is to review the responses and apply learnings. Stakeholder feedback is a valuable resource that can be used to validate the identified list of potentially material topics and inform the scoring and materiality assessment of identified impacts. It also can inform the list of potentially material risks and opportunities relating to resource use and business relationships. Stakeholder responses may raise additional questions, and in some cases, it may be appropriate to follow up for more information.

Potential challenges

An organisation’s path to effective DMA is challenging, but thoughtful planning, a carefully selected approach, and well-tailored stakeholder engagement go a long way. The DMA allows companies to identify impacts of their organisation as well as impacts on the organisation, while keeping a balance between comprehensive reporting and administrative burden. The DMA lays the foundation for the entire CSRD, and can improve how businesses strategise and make operational decisions. An effective DMA can also benefit companies’ risk management strategy, competitive advantage, and business resilience.

An organisation’s path to effective DMA is challenging, but thoughtful planning, a carefully selected approach, and well-tailored stakeholder engagement go a long way. The DMA allows companies to identify impacts of their organisation as well as impacts on the organisation, while keeping a balance between comprehensive reporting and administrative burden. The DMA lays the foundation for the entire CSRD, and can improve how businesses strategise and make operational decisions. An effective DMA can also benefit companies’ risk management strategy, competitive advantage, and business resilience.

Generally a new concept, the DMA reporting approach is still in its nascence, with limited guidance published on how to apply the concept in practice. Companies are responsible for creating their own materiality thresholds, and there are no clear limits or boundaries to the materiality assessment – it can extend up and down the value chain indefinitely. Even CSRD recognises that there isn’t a one size fits all approach, so companies need to think hard about the ESRS requirements, as well as their unique business activities and value chain. The right DMA approach is what will determine success.

Working with an advisor to generate strategies for effective DMA under the CSRD can ensure compliance and that the organisation is getting the most out of the process. 3Degrees can support companies in undergoing the DMA, or guiding them to perform their own. For details on meeting CSRD compliance or additional DMA guidance, please get in touch today.