Improving clean fuel project economics with the 45Z Tax Credit

How to maximize clean fuel incentives with 45Z Tax Credit

Get more from 45Z

Discover effective renewable energy procurement strategies in our Global Markets Report

With mounting pressure to decarbonize transportation and new policy incentives coming online, the North American clean fuels landscape is shifting. One of the most significant recent developments is the Section 45Z Clean Fuel Production Tax Credit, introduced as part of the Inflation Reduction Act (IRA). 45Z is one of 11 transferable tax credits (TTC) created as part of the IRA, and represents the growing importance of transferable tax credits as a mechanism for decarbonization.

For producers, investors, and infrastructure owners aiming to maximize the value of clean fuel projects in the second half of 2025, it is crucial to understand 45Z, how it can be paired with state and provincial Clean Fuel Standard (CFS) programs, and the ways that procuring qualifying renewable energy can increase credit values.

The 45Z Tax Credit Explained:

Understanding the 45Z Clean Fuel Production Credit

Section 45Z is a federal tax credit designed to reward the domestic production of low-carbon transportation fuels. This incentive applies to fuels produced and sold between January 1, 2025, and December 31, 2029, and provides a direct financial benefit based on the lifecycle greenhouse gas (GHG) emissions of the fuel. In short: the cleaner the fuel, the higher the credit. Key features of the 45Z tax credit include:

$0.20 per gallon for non-aviation fuels and $0.35 per gallon for sustainable aviation fuel (SAF). SAF produced after December 31, 2025 will be eligible for the same $0.20 per gallon base credit as non-aviation fuels.

Up to $1.00 per gallon for non-SAF and $1.75 per gallon for SAF if the producer meets prevailing wage and apprenticeship requirements. SAF produced after December 31, 2025 will be eligible for the same $1.00 per gallon enhanced credit as non-aviation fuels.

a. To qualify, fuels must have a lifecycle GHG emissions rate of 50 kg CO₂e per mmBTU or less, verified using approved models (such as Greenhouse gases, Regulations Emissions and Energy use in Technologies (GREET) for non-SAF and CORSIA for SAF). Read on to learn more about how biofuel producers can meet lifecycle rate requirements by procuring renewable energy.

b. Beginning with fuels generated after December 31, 2025, eligible fuels must be derived from feedstocks grown or produced in the US, Mexico, or Canada.

The credit applies to fuels produced and sold during the 2025–2029 window.

Determining Eligibility for the 45Z Tax Credit

Determining Eligibility for the 45Z Tax Credit

Not every fuel producer can claim the 45Z credit. Several criteria must be met to qualify, including that producers must register with the IRS using Form 637 and receive a signed registration letter before beginning production.

The fuel must also be produced at a facility located in the United States, and the credit is available to the entity that chemically processes feedstocks into finished transportation fuel–simple blending or compressing does not qualify. Beginning July 4, 2025, “specified foreign entities” that own or have effective control over fuel production are ineligible to earn 45z tax credits and after July 4, 2027, foreign-influenced entities are also ineligible.

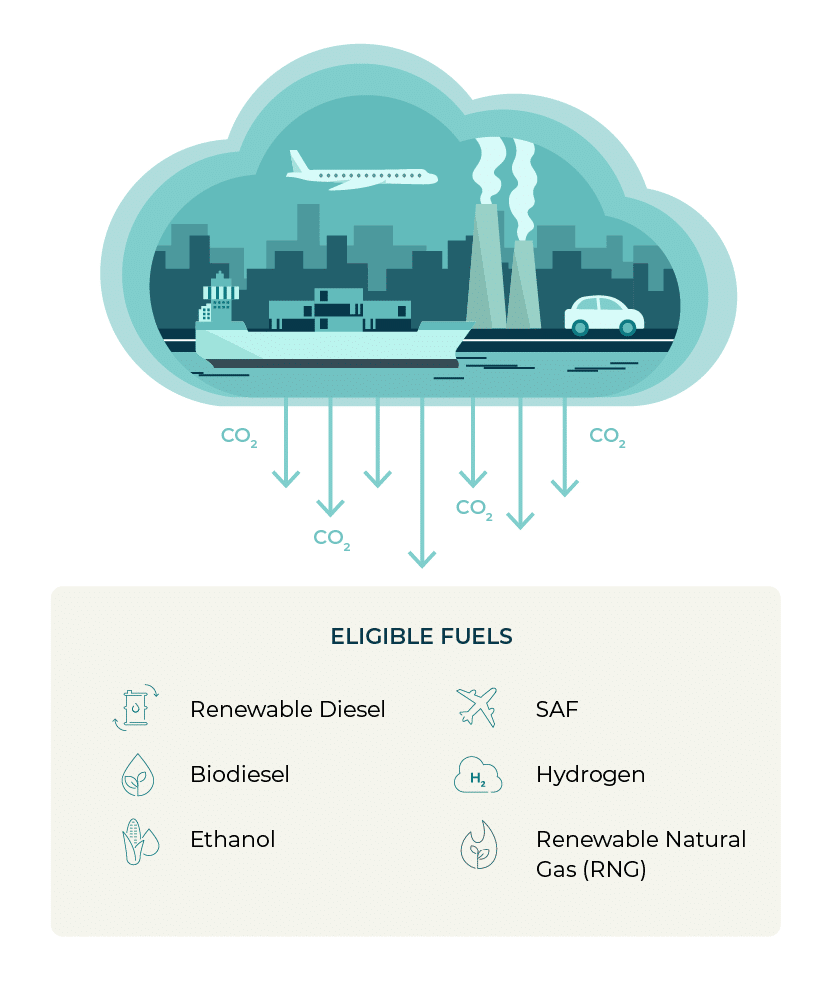

Eligible fuels include renewable diesel, biodiesel, ethanol, SAF, hydrogen, and renewable natural gas (RNG), provided they are suitable for use in transportation applications. The fuel must have a lifecycle GHG emissions rate of no more than 50 kg CO₂e per mmBTU and must be sold to an unrelated person during the credit period. Producers must maintain detailed records, and for SAF production, third-party certification of emissions is required. Beginning at the start of 2026, eligible fuels must be produced from feedstocks grown or produced in the US, Mexico, or Canada.

Beyond meeting these eligibility requirements, the 45Z credit’s transferability is a key feature for maximizing its value. Transferability allows entities that may not have enough tax liability to fully utilize the credit directly to sell their credits for cash to other entities, offering a significant advantage for organizations whose tax credits exceed their own tax obligations. The buyer of the credit can then use it to offset their own federal tax obligations.

Combining the 45Z Clean Fuel Production Credit with Clean Fuel Standards (CFS) Credits

Combining the 45Z Clean Fuel Production Credit with Clean Fuel Standards (CFS) Credits

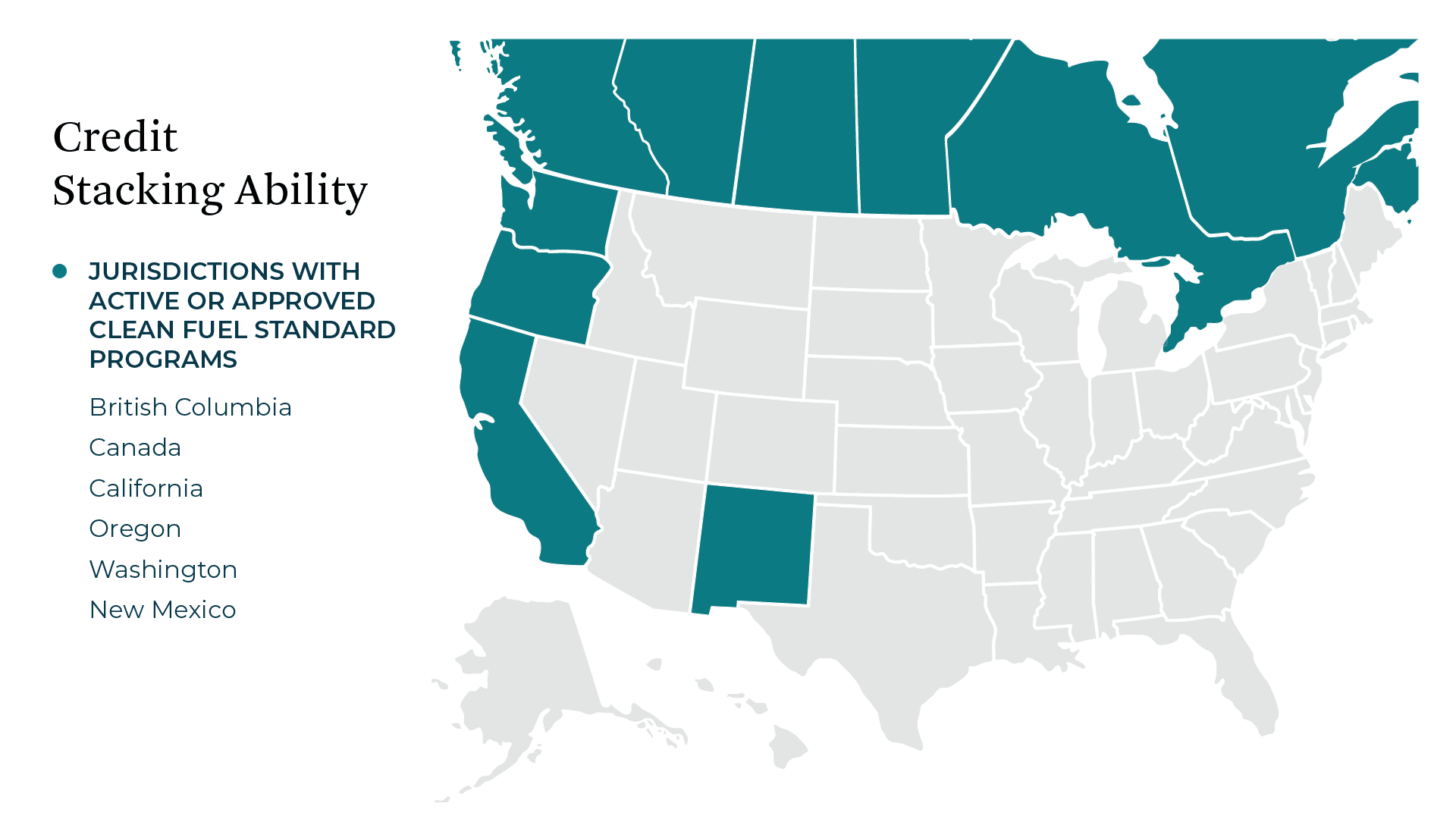

A key question for many producers is whether the 45Z credit can be “stacked” with CFS programs in California, Oregon, Washington, Canada, and British Columbia. The answer is yes—and this stacking can significantly improve project economics.

The 45Z credit is a federal incentive, while CFS programs are state, provincial, or national market-based systems. Because they operate independently, there is no conflict in claiming both. For example, a renewable diesel producer in California can claim the 45Z credit while generating valuable LCFS credits. The same holds true for similar programs in Oregon, Washington, British Columbia, and Canada.

There are, however, federal credit limitations; 45Z cannot be stacked with other federal credits, like 45Q for carbon capture or 45V for clean hydrogen production, for the same facility or fuel in the same tax year.

Maximizing Credit Value with Renewable Energy Procurement

Under the latest guidance, clean transportation fuel producers may use low-carbon inputs consistent with the guidelines established in the 45V Clean Hydrogen Regulations to reduce the GHG emission rate of their fuel and maximize their tax credit generation opportunity. One such method is using qualifying energy attribute certificates (EACs) to achieve a lower GHG emissions rate associated with the production of eligible transportation fuels.1

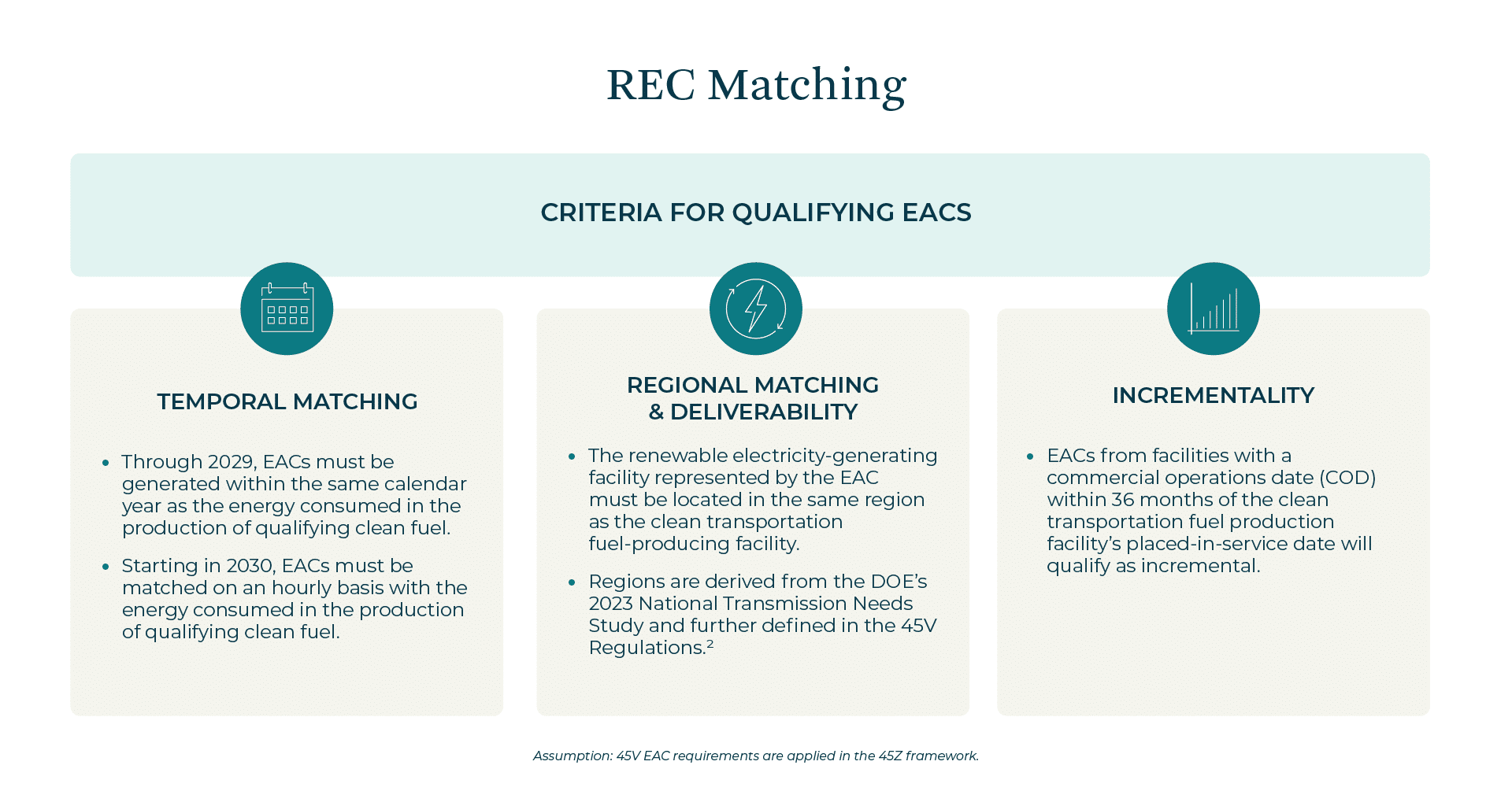

Qualifying EACs must meet the same temporal matching, regional matching, and incrementality criteria as defined in the 45V Regulations.2 Though additional regulation is needed to clarify how the 45V structure will apply entirely to the 45Z credit, the framework established by the 45V regulations give us a general idea:

EACs must be generated within the same calendar year as the energy consumed in the production of qualifying clean fuel through 2029, and hourly matching is not required until 2030, beyond the current expiration of the 45Z credit.

The renewable electricity-generating facility represented by the EAC must be located in the same region as the clean transportation fuel-producing facility. Regions are derived from the DOE’s 2023 National Transmission Needs Study and further defined in the 45V Regulations.3

EACs from facilities with a commercial operations date (COD) within 36 months of the clean transportation fuel production facility’s placed-in-service date will qualify as incremental.

Strategic Implications and Opportunities of the 45Z Clean Fuel Production Credit

The ability to combine 45Z with CFS credits creates significant opportunities for project developers and owners. By leveraging both 45Z and CFS credits, producers can unlock multiple revenue streams, making low-carbon fuel projects more financially attractive. Both 45Z and CFS programs require rigorous emissions verification and documentation, often relying on third-party certification to ensure compliance. While stacking is currently allowed, producers should monitor legislative developments that could affect eligibility or credit values.

Using qualifying energy attribute certificates (EACs) – that meet the same temporal matching, regional matching, and incrementality criteria as defined in the 45V Regulations – can offset the underlying electricity used in the production of eligible fuels. Thus, under the 45Z, renewable energy matching can yield a lower GHG emissions rate, and increase credit values. Similarly, renewable energy certificates (RECs) can also be applied under three of the CFS programs (Oregon CFP, Washington CFS and California LCFS) to reduce the fueling CI and increase the numbers of credit generated.

The Section 45Z Clean Fuel Production Credit represents a major opportunity for U.S. clean fuel producers, especially when combined with regional CFS programs and qualifying renewable energy procurement. By understanding the eligibility requirements and stacking rules, producers can accelerate the transition to low-carbon fuels while maximizing financial returns. As the domestic policy landscape continues to evolve, staying informed and agile will be key to success in the clean fuels market.

45Z was recently amended by Congress and may change further depending on any resulting regulatory adjustments. 3Degrees’ Regulatory Team will continue to monitor the progression of policies that may amend the 45Z credit and will provide future updates.

1. An input for “Imported Renewable Electricity: EACs” is included in the DOE’s 45ZCF-GREET Model used to calculate lifecycle emissions of clean transportation fuel production.

2. Based on the 45V credit framework and the directions in the 45Z notice of intent that the GREET model should apply “rules similar to the rules under section 45V” we’re assuming this is how the EAC requirements would apply in the 45Z framework.

3. Regions are based on the U.S. Balancing Authority to which the fuel generation facility and renewable energy generation facility are electrically interconnected (not necessarily their geographic location), with each Balancing Authority linked to a Region. For more information, see DOE’s 45ZCF-GREET User Manual.

Beginning with a sustainability-first approach, 3Degrees’ team of climate experts analyze a vast range of renewable energy options to ensure that clients meet the complex eligibility standards set forth by the 45Z tax credit. We start with sustainability departments, emphasizing that tax credit deals aren’t just financial transactions, but an opportunity for meaningful climate action. Working cross-functionally across sustainability and finance, our team of experts leverages industry-leading renewable energy procurement to help identify the best opportunities for your business’s unique energy requirements.

Learn how we can deliver confidence and value for your clean fuel strategy by getting in touch below.

Ready to get started?