Filter Insights by:

We examine the challenges companies face in meeting near-term supply chain emissions targets amid lagging updates to major climate standards, explore best practices for applying market-based accounting approaches to supply chain decarbonization, and introduce our Supply Chain Emissions Reduction solution.

Our Global Market Insights Report is here! Subscribe now to receive it in your inbox.

Learn how to improve your CDP score through strategic energy-related action and disclosure.

As companies work toward net zero, biomethane is becoming a vital decarbonisation tool. In this episode of our biomethane series, we explore key opportunities and risks to help corporate buyers make informed decisions.

Learn how 3Degrees helped a data center company tackle its APAC strategy on its path to procure 100% renewable electricity globally by 2030.

Learn about the key outcomes from last month's meeting of private and public sector leaders at COP29,

Explore the impact of negative electricity prices and geopolitical shifts on Europe’s energy market in the second half of 2024.

Watch as we explain some supplier action tools and tactics in our latest Climate Leadership Series video.

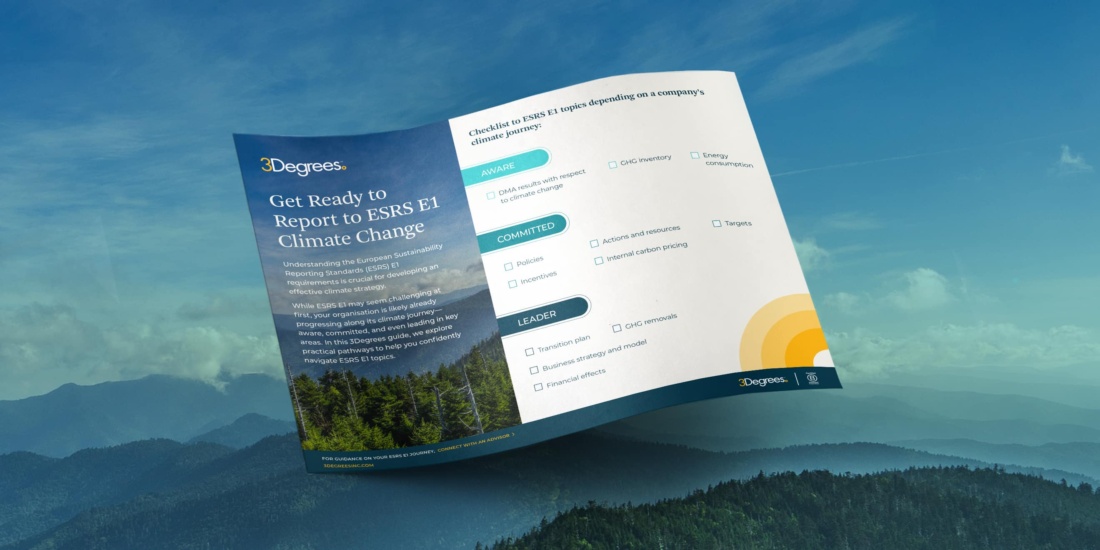

As businesses navigate the complexities of ESRS E1 topics, having a clear plan aligned with your organisation's climate journey is key to long-term success.