In a bold stride towards combating climate change, the European Union (EU) rolled out the transitional phase of the Carbon Border Adjustment Mechanism (CBAM) in October 2023. Ahead of that move, the EU Commission adopted a CBAM implementation regulation, defining reporting obligations for the transitional period. This ushers in a new era of mandatory stringent reporting for corporations involved in importing and exporting CBAM goods in the EU. The transitional phase lasts just over a year, so affected EU corporations must adapt quickly to avoid noncompliance penalties.

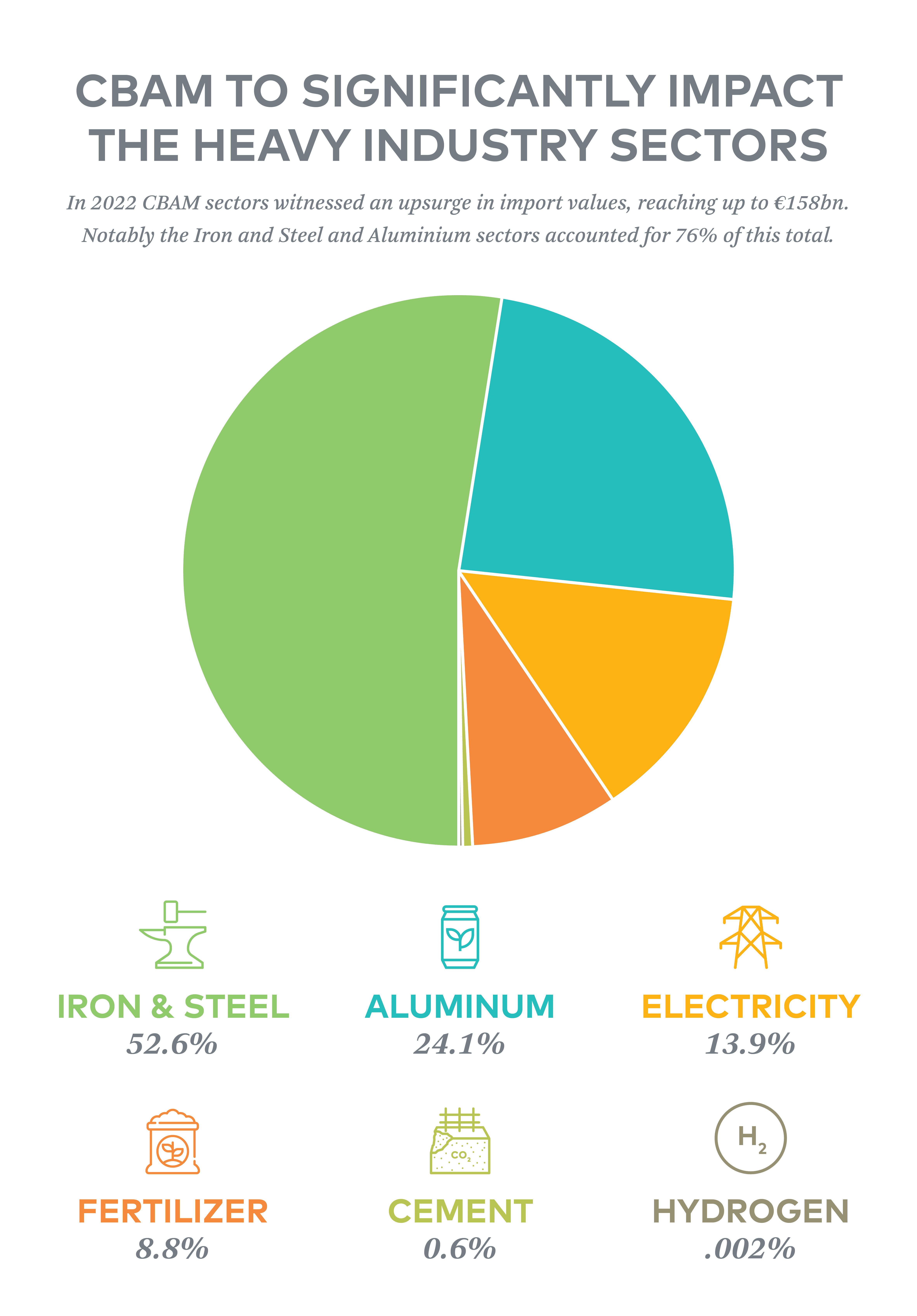

This specifically affects the following designated carbon-intensive CBAM sectors, but there are plans to widen the scope in the future:

- Iron and steel

- Cement

- Hydrogen

- Aluminium

- Fertilisers

- Certain precursors (e.g., basic materials used in inputs in the production of CBAM goods)

- Electricity

- A limited number of downstream products (e.g., screws and bolts of iron and steel)

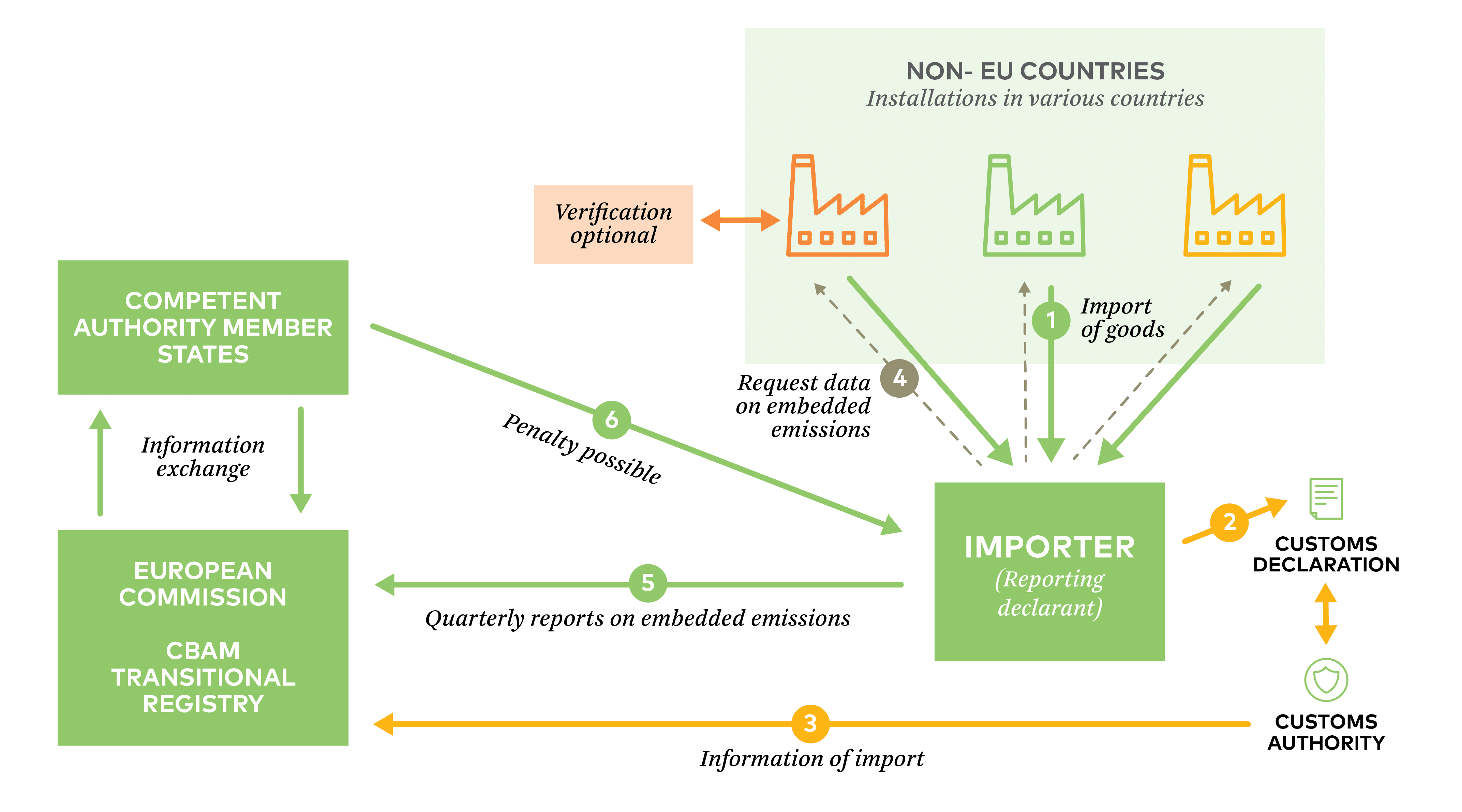

The implementation regulation includes provisions for the establishment and operation of a CBAM Transitional Registry that importers in the affected sectors must utilise to submit their CBAM reports.

Understanding the CBAM Transitional Phase Landscape:

During the transitional period, importers in CBAM sectors are required to submit quarterly reports detailing both direct (scope 1) and indirect (scope 2) emissions embedded in imported goods, alongside any carbon price paid abroad for these emissions. The first of such reports is due for submission to the CBAM Transitional Registry by 31 January 2024 for imports occurring in Q4 2023. Below are the key transition phase dates:

Categories of Reporting Declarants:

The regulation identifies three categories of reporting declarants:

- Self-reporting importers: Submit customs declaration on their own behalf.

- Authorised importers: Have special authorization to submit customs declaration on behalf of others (e.g. a large multinational corporation that has received special authorization from the customs authorities to handle customs declarations on behalf of its subsidiaries or associated companies).

- Indirect customs representatives: Act as third-party representatives for importers, especially when the importer is not EU-based (e.g.typically third-party logistics providers, customs brokerage firms, or freight forwarders that offer customs declaration services as part of their portfolio).

What to Include in a CBAM Report

CBAM reports should encompass a range of information that’s broken down into four categories.

Imported goods:

- Quantity of goods imported (expressed in MWh for electricity and in tonnes for other goods)

- Type of imported goods identified by their specific product code (CN code)

- When reporting on electricity as imported goods, the declarant must include the following:

- The emission factor for electricity, expressed as tonne CO2e/MWh

- The data source and method used for determining the emission factor of electricity

Embedded emissions:

- Country of origin of imported goods

- Installation data from where the goods were produced

- Production routes used that specify the technology used for the production of the goods

- The specific embedded emissions of goods (sum of scope 1 and scope 2 emissions associated with the production of a good)

Embedded indirect emissions:

- Electricity consumption per tonne of goods produced in MWh

- Indication of whether the declarant reports actual emissions or default values as published by the EU Commission

- The corresponding emissions factor used for electricity

- The amount of specific embedded indirect emissions

Carbon price:

In cases where corporations import goods from a country with an established carbon price the following should included in the report:

- Carbon price type, imposing country and monetary value

- Type of CBAM good

- Compensation available in the country that could result in a reduction of the carbon price.

- Quantity of embedded emissions covered by the carbon price

- Quantity of embedded emissions covered by rebate or free allocation

- An indication of the provision of a legal act providing for the carbon price

Once finalised, importers must submit their reports to the newly established CBAM Transitional Registry which will be managed by the EU Commission.

Non-compliance carries hefty penalties, ranging from €10 to €50 per tonne of unreported embedded emissions. The competent authorities in Member States will determine precise penalty amounts, making it crucial for corporations to prioritise compliance.

What Lies Beyond the CBAM Transitional Phase?

The transitional phase is a lead-up to CBAM’s full implementation on 1 January 2026. After this, CBAM reporting changes from quarterly to annual, with importers buying and surrendering yearly CBAM certificates through the registry, reflecting GHG costs of imported goods. CBAM certificate prices will match average weekly EU ETS auction prices, as CBAM phases in while free EU ETS emission allowances phase out. After the transitional phase, third-party emissions data verification is mandatory, emphasizing accurate reporting from the outset, even when verification isn’t required.

Implications for Corporations

The CBAM regulation signals a major shift urging corporations to overhaul their supply chain management and data exchanges. Importers must deepen ties with suppliers for essential data and implement systems to track and report GHG emissions. This necessitates significant technological and human resource investments. CBAM’s financial impact from 2026, could escalate corporate import costs, altering cost frameworks. Companies not reducing supply chain emissions may face heightened costs, affecting competitiveness. Corporations must address emissions with current suppliers or find lower-emission alternatives. Proactive EU exporters investing in low-carbon solutions will likely have a competitive edge. Notably, CBAM’s scope is set to expand by 2026, urging all corporations to prepare.

Preparing for CBAM

CBAM is a testament to the EU’s unwavering commitment to climate action to reach its ‘Fit for 55’ climate neutrality goals. It necessitates a paradigm shift in how businesses operate within and outside of the EU. As we enter the CBAM transitional phase, the onus is on corporations to understand the intricacies of the CBAM regulation, align their operational frameworks accordingly, and foster a culture of compliance and sustainability.

Want to learn more about the CBAM landscape?

The 3Degrees’s Energy & Climate Practice team is ready to provide the requisite support and guidance to navigate through the CBAM landscape. Get in touch with our team to learn more.