Why PPAs are popular procurement options for corporate and industrial buyers

Explore this article to understand the fundamentals, benefits, and considerations of Power Purchase Agreements and Virtual Power Purchase Agreements.

Interested in more on PPAs?

Sign up to download our upcoming Global Market Insights Report.

The renewable energy procurement landscape has changed dramatically in recent years in large part due to the increasing pool of potential buyers driven mainly by commercial and industrial (C&I) organizations. This buyer pool has wider, easier access to an array of procurement options and is implementing renewable energy at a record-breaking pace. While there are other options available, power purchase agreements (PPAs) have become the method of choice for many C&I organizations to achieve large scale emissions reductions.

But deciding if PPAs are right for your organization can be complex. This article helps lay the foundation to answer this question by exploring the procurement of renewable energy through PPAs, both physical and financial (virtual)*. Both types of PPAs can be powerful tools to help companies develop robust clean energy portfolios and achieve sustainability goals. However, they do differ in a number of significant ways, and this article identifies these differences and other factors to consider when evaluating PPA opportunities.

Interested in more on PPAs?

Sign up to get access to 3Degrees’ Global Market Report and subscribe to future editions of to keep track of market trends and their effects on the energy and PPA market landscape globally.

What is a Power Purchase Agreement (PPA)?

A PPA, at its core, is a contract between two parties where one party sells both electricity and renewable energy certificates (RECs) to another party. In corporate renewable energy PPAs, the “seller” is often the developer or project owner, while the “buyer” (often called the “offtaker”) is the C&I entity. C&I renewable energy PPAs can take two primary forms – physical or financial (the latter often referred to as “virtual”). The best structure for an organization depends on the markets where the offtaker is located and where projects are available, as well as the goals, priorities, and risk tolerance of the offtaker.

Physical PPAs

Physical PPAs are most commonly used by organizations that have heavy, concentrated load in a specific location or grid region (e.g., data centers). This is because under a physical PPA, the seller delivers the renewable electricity to the offtaker, who actually receives and takes legal title of the energy. Physical PPAs are best suited for competitive retail or direct access energy markets, such as Texas, Illinois, and California. They are possible – but significantly more difficult – in a regulated market. A physical PPA is structured as follows:

- The offtaker buys renewable energy directly from a seller.

In a typical renewable energy PPA, the developer builds, owns, and operates the renewable energy project, and sells the output to the buyer at a specified delivery point. - The offtaker takes title to the energy at the delivery point, as well as associated RECs.

- The offtaker is responsible for moving the energy away from the delivery point to its load, typically done through 3rd-party service providers.

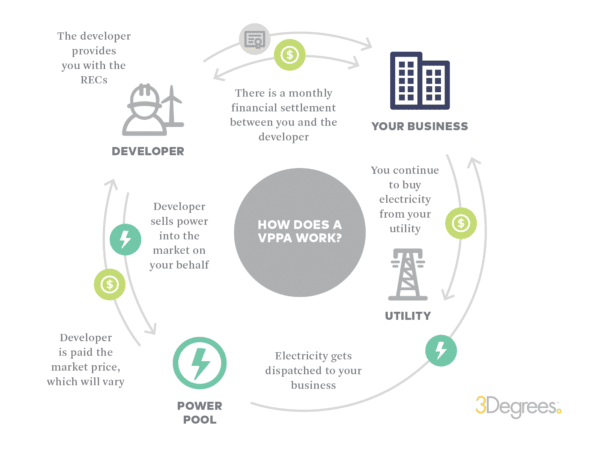

Virtual (Financial) PPA or VPPA

Unlike a physical PPA, a virtual PPA (VPPA) is a financial contract rather than a contract for physical power. The offtaker does not receive, or take legal title to, the electricity and in this way, it is a “virtual” power purchase agreement.

In a VPPA, an offtaker agrees to purchase a project’s output and associated RECs at a set fixed price. The developer then liquidates the energy at market pricing and passes the revenue through to the offtaker. More specifically:

- Similar to a physical PPA, the seller in a VPPA is oftentimes a developer who builds, owns, and operates a project and delivers the energy output to the specified delivery point.

- The offtaker agrees to pay the seller a fixed price for renewable energy delivered to a specific point, typically a market hub or project busbar. This fixed price is the guaranteed price the developer will receive – no less and no more – irrespective of the floating market price.

- The seller generates and liquidates a project’s energy at market pricing. When the floating market price exceeds the fixed VPPA price, the developer passes the positive difference to the offtaker. When the converse is true – the market price is below the VPPA fixed price – the offtaker must pay the developer the difference.

- The offtaker retains all of the RECs associated with the delivered energy, as long as that is specified in the contract.

This type of structure is called a contract for difference (CFD).

In this way, the seller is guaranteed a fixed price for the output it sells – which is critical for developers that are looking to finance new projects. These projects can be particularly attractive for buyers that want to contribute to the development of new renewable energy resources and that have electricity load that is widely dispersed.

VPPAs are typically only available in organized markets such as a regional transmission organization (RTO) or independent system operator (ISO), which serve as third-party independent operators of the transmission system, ultimately responsible for the flow of electricity within its domain. This is for two important reasons:

- First, VPPAs require market liquidity – where the developer, an independent power producer (IPP), is permitted to sell its power directly into the grid. This is the case in RTO/ISO regions, but not necessarily so in a vertically integrated market where a single entity is responsible for the generation, transmission, and distribution of electricity.

- Second, the economics of a VPPA hinge on the difference between the floating market price and the VPPA price. RTO/ISO regions have publicly available market pricing that serves as the basis for calculating VPPA financial settlements.

Importantly, because no energy actually changes hands, the VPPA offtaker does not need to make any changes to how it purchases the electricity required for its operations.

Why enter into a PPA?

There are three primary benefits of a PPA, regardless of whether it is physical or virtual:

PPAs can provide a hedge against future energy fluctuations. In a physical PPA, the hedge value is realized because the cost of the purchased volume of electricity is kept flat at the PPA rate while standard electricity rates tend to increase over time. In a VPPA, the value is realized when revenues from the VPPA increase because market pricing has risen above the PPA price – offsetting similarly rising retail electric rates. It’s important to remember though, a hedge instrument is not intended to create upside but rather to manage downside exposure. Be wary of VPPA projections that show hockey stick-shaped forward energy price curves promising high net present values (NPVs).

Both wind and solar projects have zero associated emissions and generated RECs apply to the Greenhouse Gas (GHG) Protocol scope 2 market-based reporting methodology. And, if the PPA is for a new-build project, offtakers can easily and credibly claim that they are helping to add new renewable energy to the grid (many use the term “additionality” to describe this) – a level of impact beyond simply purchasing RECs from an existing project.

PPAs are a well-understood renewable energy procurement mechanism that can be shared with internal and external stakeholders. They also move the needle on a double bottom line – helping to achieve important corporate environmental goals while also making a positive impact on the grid through the addition of new renewables, which makes for powerful brand and marketing narratives.

[inlinetweet prefix=”Why enter a PPA?” tweeter=”@3Degrees_Inc” suffix=”Read more”]PPAs have financial, environmental, and marketing benefits.[/inlinetweet]

Physical vs. Virtual*

Despite these shared benefits, physical and virtual PPAs do differ in some material ways:

Physical PPAs require that the offtaker obtain power marketing authority from the Federal Energy Regulatory Commission (FERC) to purchase wholesale power from the power producer. While not insurmountable, doing so may be outside of the offtaker’s core business or simply be too time-consuming. An offtaker can engage a third party already authorized to buy power at wholesale, serving as the market participant. This, of course, has its own risks (see below). Because no power is changing hands in a VPPA, the offtaker does not require FERC authority.

Depending on which accounting standard your company uses, a VPPA may be considered a derivative, which requires more complex accounting treatment. Generally VPPAs are not considered derivatives under U.S. GAAP, while they typically do qualify as derivative contracts under IFRS.

Physical PPA offtakers need to consider what happens with the energy once they receive and take title to it and find a solution to move the purchased energy to the offtaker’s locations, requiring transmission, distribution, and delivery. C&I offtakers typically contract with third party providers for these services because perfectly syncing the deal terms of these services (typically limited to a couple to several years) with those of longer-term PPAs is unlikely and can add a compounding layer of risk and complexity to the overall transaction.

As mentioned above, physical deal structures where the energy is delivered to an offtaker’s facility are limited to competitive retail markets (i.e., PJM, Northeast, ERCOT and other isolated states in MISO and WECC). VPPAs have broader potential, possible in any RTO or ISO. Furthermore, because VPPAs are financial in nature and don’t involve moving electricity, they are not inherently location-dependent. This means offtakers can find the most attractive project and not be limited to projects located within its immediate region. It also allows offtakers to consolidate their country-wide demand to capture economies of scale.

PPAs require learning on multiple levels for an organization, as VPPAs tend to be a new procurement mechanism for most offtakers, requiring education on technical and non-technical topics alike. Not to be under-estimated, VPPAs require cross-departmental coordination within organizations and strong stakeholder alignment. Once a VPPA is in place, new processes will need to be developed to manage the long-term contract and the monthly financial settlements. All this takes time, effort, and persistence.

Each of these factors should be considered when evaluating PPA opportunities.

[inlinetweet prefix=”Physical vs. Virtual PPAs:” tweeter=”@3Degrees_Inc” suffix=”Read more”] PPAs and VPPAs have important differences. [/inlinetweet]

Risky business?

Although PPAs are increasingly common among the C&I segment, they require a buyer that can get comfortable with the specific risk profile of this contract type. There are tradeoffs in every deal structure, and special attention should be paid to the following risks and potential mitigation measures.

- Energy Market Risk: In a VPPA, the primary risk factor that a buyer must get comfortable with is wholesale electricity market risk, which is not something that most corporates are familiar with as part of their core business. Because a VPPA’s value is based on a floating wholesale electricity market price, the importance of understanding the forces which can affect that price – and drive it up or down – can’t be overstated. Factors that can impact future electricity pricing include:

- Changes in electricity demand

- Natural gas pricing

- Energy capacity additions and retirements (renewable and conventional)

- Transmission and distribution upgrades

- The regulatory environment

- Extreme events / severe weather occurrences

- And more

- Project Development risk: Most often, C&I buyers are looking to contract for a new build renewable energy project, which means there is always the risk that the project developer will not ultimately get the project built, or that it cannot be built on the developer’s original budget or timeline. Typically project financing and construction takes between 18 to 24 months after a PPA contract is signed, which doesn’t include the time already spent to execute the deal. With the amount of effort to get a PPA in place, Buyers will want to mitigate as much of this risk as possible, which means fully vetting the project development progress to-date as well as the track record of the developer.

- Contracting risk: The PPA itself is a very large and complex contract that requires in-depth negotiations between the C&I buyer and renewable project developer on many key commercial and legal terms. As PPA market dynamics are always shifting based on the supply and demand for projects, so too are the specific terms that buyers and sellers are willing to agree to. It is important for Buyers to understand the implications of these key commercial terms, since they have a material impact on the financial value of the PPA as well as the overall amount of risk that the Buyer is taking on.

Offtakers should have a clear understanding of all the risks associated with a PPA transaction so they can make informed decisions based on the potential outcomes, ultimately structuring a transaction in line with their specific risk tolerance.

The importance of a trusted advisor

Both physical and virtual PPAs offer a strong environmental impact story to C&I organizations, and they can be more financially attractive than alternative options – however, they do come with material complexity and risk. Corporate VPPAs have become increasingly common in today’s market but they are not the right fit for every organization. We recommend working closely with a trusted advisor to determine the best option(s) for your organization.

Interested in learning more about PPAs and VPPAs? Get in touch today to start the conversation.

*Due to legal and regulatory restrictions in certain jurisdictions, this material is only intended to be accessed in those jurisdictions where to do so would not constitute a violation of the local marketing laws. This material is provided as general information only. It does not constitute an offer to sell or the solicitation of an offer to buy any investment. Nor does it constitute the giving of investment advice. For more information click here.

Get more insights on PPAs by downloading our Global Market Insights Report and subscribing to future editions.

Suggested Insights

Explore more of our latest climate insights.

SBTi V2.0 enforces stricter corporate climate rules. Discover the critical decisions your team should make before February 1, 2027.

Discover what biochar is used for in our infographic depicting the product's lifecycle.

Watch a practical session exploring how biomethane can help tackle both your scope 1 and scope 3 decarbonisation efforts.