The first consultation on the UK’s Review of Electricity Market Arrangements (REMA) concluded in October 2022 and the results are in. After digesting the results, the UK Government’s Department of Business, Energy and Industrial Strategy (BEIS) published its summary of the feedback they received on their proposal for reform, and for those of you who do not have the time to review its 129 pages of content, it seems that most respondents agree that the market needs reform.

However, before we dig into what’s still up for discussion and what has been ruled out, let’s recap on REMA and its aims.

REMA: Background and steps taken so far

In the summer of 2022, and in response to the recent energy crisis, BEIS announced its intention to redesign the current UK electricity market to enable it to better accommodate future challenges presented by the transition to a distributed renewable energy system.

In addition to addressing the ever elusive energy trilemma, which is the challenge of simultaneously promoting sustainability, affordability, and security of supply, the priorities of the reform were:

- increasing investment in low carbon generation capacity in order to meet decarbonisation targets;

- increasing system flexibility to support the balancing of supply and demand and the stability of the system as variable renewable generation increases;

- providing efficient locational signals to minimise system costs;

- maintaining system operability as variable renewable generation increases;

- and managing price volatility as variable renewable generation increases.

The reforms will be focused on the wholesale power market, specifically looking at pricing location, technology, balancing, price formulation, and dispatch method, as well as the acceleration of low carbon power generation while promoting flexibility, capacity and operability. BEIS made it clear that they were willing to consider a broad range of solutions and were not shy to acknowledge that reform on this scale will inevitably result in both winners and losers.

To solve the problems presented by the green transition, there were a variety of ideas on the table from locational marginal pricing to market segmentation by technology, to even a Dutch style auction by carbon abatement potential.After the first round of consultation, we are a step closer to the new target market.

The consultation received over 200 responses from a range of interested parties, including renewable energy developers, utilities, trade associations, members of academia, investors and even 29 private energy enthusiasts. BEIS assessed the feedback they received and triaged ideas based on its priorities, outlined above, so let’s have a look at the results.

What’s out…

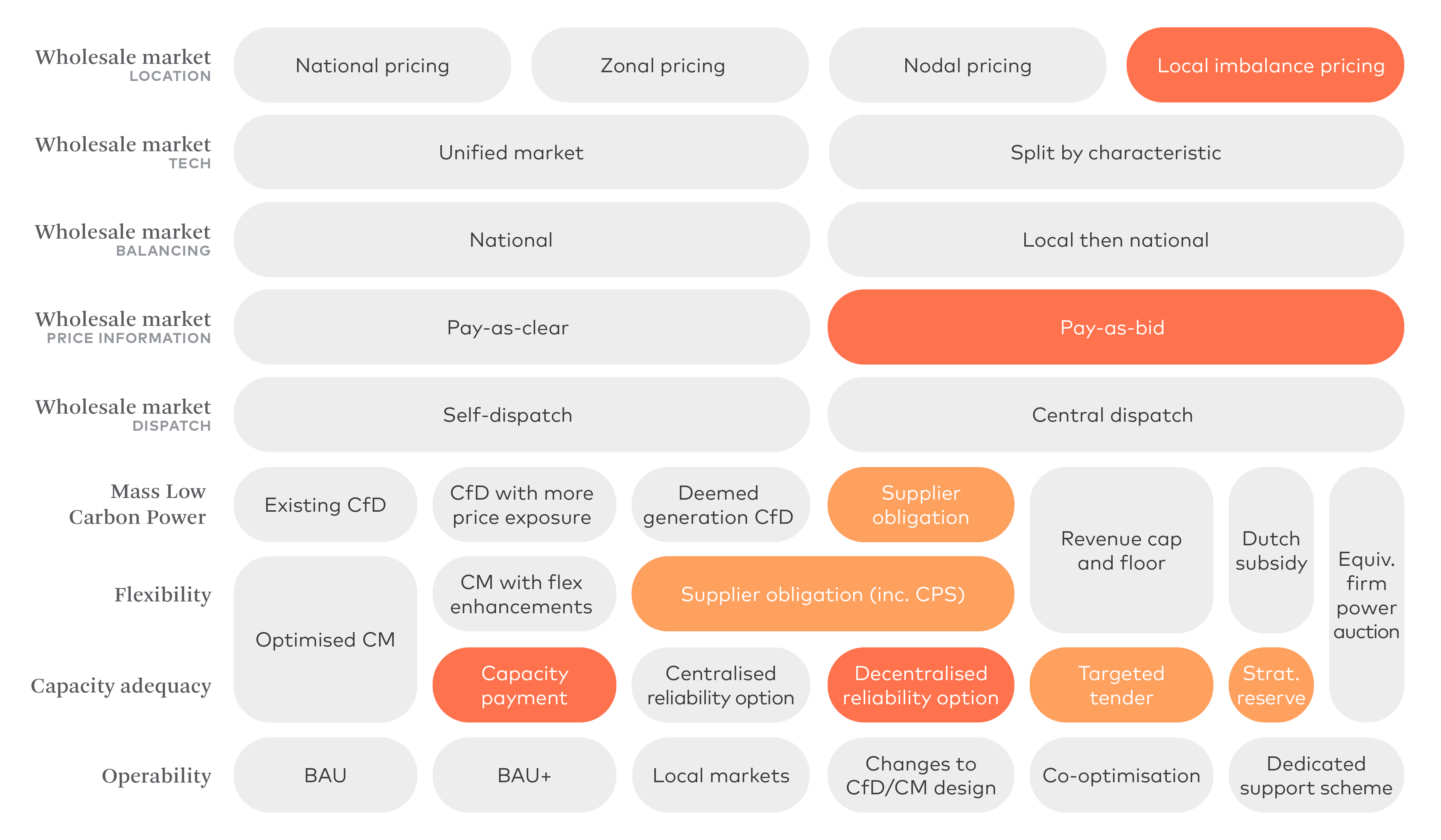

A map of the options space highlighting options discounted based on consultation feedback.

A number of proposals were eliminated, and a summary of the important ones is below.

Local imbalance pricing

The proposal for setting imbalance prices locally based on the specific supply/demand balance for a particular part of the grid did not make it to the next round of consideration. BEIS concluded that this idea would be too complicated to implement and would not result in the cheapest option for the consumer.

Pay As Bid price formation

The “Pay As Bid” option for generators to offer individual bids each half-hour of the day has been eliminated due to the significant complexity and concern around the possibility of generators gaming the system to the detriment of consumers. So, “Pay as Clear” is here to stay, which means that other reform proposals must prevent lower marginal cost generators from achieving elevated prices during periods of system stress.

Increasing supply obligations to support Mass low carbon generation

BEIS ruled out the idea of placing further obligations on suppliers to support renewable energy deployment in the short-term, presumably in recognition of the stress energy retailers and consumers are already under. This implies that further renewable energy deployment must rely on consumer demand, corporate power purchase agreements (PPAs), or government support funded by taxpayers.

Capacity payment

BEIS ruled out the option of offering capacity payments to generators due to the lack of evidence that was put forward to justify any additional benefits compared to the current auction-based capacity market, however BEIS appears open to reviewing the existing scheme and will likely seek additional input in future REMA consultations.

What is left in…

Market separation

BEIS is still considering moving renewable energy generators to their own dedicated market which would likely be based on project-specific financing and construction costs, though price setting details have yet to be defined. The most likely settlement mechanism for this market would be a Contract for Difference (CfD) with additional market exposure such as the establishment of caps or collars and could use deeming for settlement purposes meaning that CfD adjustments are calculated based on a generic generation profile rather than project-specific data.

Potential impact on corporate buyers

This would likely negatively impact the corporate PPA market, as it will be hard for corporate buyers to demonstrate true additionality if a project’s market risk is borne by the government, meaning subsidised, while the corporate receives the REGOs. Further, there would be limited potential upside for corporate buyers in any PPA contracts due to it going to the government through their CFD.

Moving to locational marginal pricing

Moving to zonal settlement or a US-style nodal pricing system are still very much on the table as alternatives to the current national settlement system. Respondents highlighted the complexity involved in developing these markets and the potential damage it could do to investor confidence. BEIS, however, is likely eyeing the possible benefits of lowering the wholesale price of energy in areas of high renewable penetration, as it could offer both regional industrial incentives and lower domestic power costs for rural areas of the country.

Potential impact on corporate buyers

This would likely negatively impact existing virtual PPAs and would make the siting of new projects much more important, as areas of high renewable deployment would likely see much lower settlement prices. BEIS should consider this option carefully as it could have the unintended consequence of slowing down large-scale renewable deployment, as permitting and interconnection would likely be harder to achieve in areas of high demand which tend to be near urban areas.

Wholesale Balancing

BEIS has not yet ruled out the idea of balancing the system at the local level before the national price settlement, with some respondents making the case that it could reduce the number of grid operator interventions required and reduce the likelihood of stress events due to supply/demand dynamics largely being sorted out earlier in the balancing process.

Potential impact on corporate buyers

This would likely negatively impact the corporate PPA market due to increased balancing costs in areas of high renewable deployment, as intermittent generation requires more balancing actions. Corporates with physical PPAs would suffer most, as these agreements expose them to balancing costs. In virtual PPAs, developers are typically the party exposed to balancing costs, so they would likely require higher PPA prices to cover this risk in new contracts and may call upon change in law clauses in existing contracts.

Supporting the rollout of “Mass low carbon power”

As noted above, BEIS was not open to additional schemes for suppliers to support renewable energy deployment, however respondents were keen to expand the current CfD mechanism while taking care not to weaken the growing corporate PPA market. In BEIS’ response, it recognised the comments around supporting the PPA market and was open to the possibility of the government standardising and underwriting PPA contracts to help reduce counterparty risk and stimulate more PPAs.

Potential impact on corporate buyers

The impact on the corporate PPA market should be positive. The fact that BEIS has not signalled an intention to increase government subsidies to renewables highlights the importance of corporate PPAs in the UK market, which is reflected in their stated intention of supporting the corporate PPA market, which should also improve investor confidence.

Dispatch methods

Moving to a centralised dispatch model where the grid directly calls generators on or off as opposed to allowing market signals to incentivise the required behaviour was seen as cumbersome and technologically difficult, but it was not ruled out. It was noted that continuing to use market signals to encourage self-dispatch stimulates adjustments in real-time, so we may see the central dispatch proposal fall away in the next consultation.

Potential impact on corporate buyers

Moving to a centralised dispatch model would likely negatively impact the corporate PPA market, as it distorts market-based solutions to curtailment. In theory, a centralised model shouldn’t significantly alter the amount of renewable energy curtailed during periods of oversupply, but there is a risk that the grid operator would be choosing winners and losers rather than allowing buyers and sellers to agree to terms themselves.

Overall expected impact on Corporate PPAs

Despite getting more clarity on BEIS’ thinking around REMA, the future of the UK wholesale power market is still far from certain. Any proposal that changes the fundamental pricing mechanism will clearly have significant impacts to current and future CfDs and PPAs, however more subtle changes to things like balancing and dispatch could also have severe implications to these agreements.

Moving renewable energy assets to their own dedicated market would also present problems to CfD-based corporate PPAs, especially if the government used their own CfD mechanism to set the price of this market. After all, how would a corporate buyer compete with a government-backed CfD available to all renewable energy assets in the UK? Typically by paying higher PPA prices that may stymie the corporate PPA market.

As mentioned above, BEIS has openly accepted that there will be winners and losers with a change of this scale, but some comfort can be taken in their stated intention to protect the growing UK PPA corporate market, though it is certain that corporates and developers alike will be keeping a keen eye on the results of the next consultation.

Next steps

BEIS expects to publish a second consultation by the end of 2023, and this one is intended to provide an opportunity for stakeholders to provide further input and feedback on the proposed reforms to the electricity market. The government has indicated that they may still make decisions on shorter-term reforms if they are required to protect consumers. However, it seems unlikely BEIS will need to make any rash decisions given current market prices.

BEIS recognizes the need to consider the potential impacts on consumers and establish an “end-user forum” to address this. This forum will allow consumers to provide their perspectives and feedback on the proposed reforms, ensuring that the reforms are consumer-centric and consider the affordability and accessibility of energy for all.

3Degrees will continue to monitor this consultation and release further publications as the initiative unfolds. In the meantime, feel free to get in touch to further discuss this topic and how it may affect your current PPAs or upcoming procurements.