The Science-Based Targets Initiative (SBTi) has recently released a package of consultation documents aimed at financial institutions, including the conceptual framework for the Net-Zero Standard for Financial Institutions (“FINZ”). The document is neither an exposure draft nor the final standard, but serves as an important milestone along the way to their expected publication in Q4 2023 and in 2024, respectively.

We have gleaned two major takeaways from the FINZ conceptual framework. First, much work lies ahead for SBTi before a FINZ draft will be ready for exposure. Specific definitions, metrics, methods, and examples are still works in progress and will need significant fleshing out before publication of the final standard. The consultation document is also full of optionalities that are open for comment, such as whether financial institutions should aim for 90%, 95%, or 100% net zero-aligned finance.

More important, though, is our second takeaway – regardless of the decisions SBTi makes with the minutiae of the final validation criteria, this conceptual framework makes the ultimate destination clear: full decarbonization of the economy by 2050. SBTi acknowledges that the financial sector will be a key player in that transition, and has repeatedly noted that reducing exposure through divestment or portfolio shifting will not be adequate. Engaging portfolio companies to drive decarbonization will be the only credible path forward.

In this article, we’ll examine what the concept of net zero means for the financial sector and what financial institutions looking to set a science-based target (SBT) should consider.

Transition to net zero will mean a paradigm shift for the financial sector

A transition to net zero will require financing to be diverted out of high-emitting activities (such as oil and gas) and into new and emerging ones (such as carbon removal). This presents a complete business model redesign, particularly for asset managers who operate in accordance with client mandates and banks that have diversified lending policies due to lending limits and liquidity requirements.

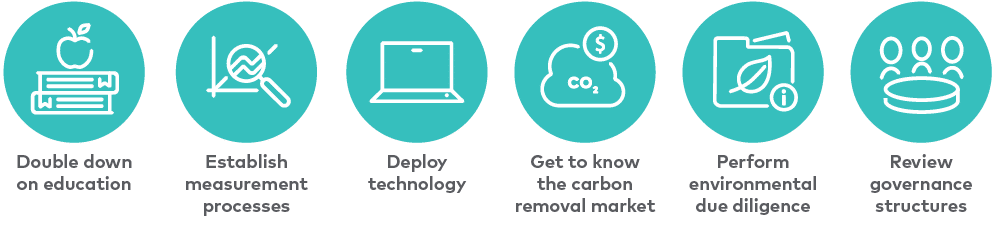

Practically, financial institutions considering setting an SBT or otherwise adopting a 1.5C-aligned strategy should start taking the following steps:

Most sustainability professionals at financial institutions are currently focused on the sustainability performance of their products (e.g., ESG funds) and/or climate risks (e.g., the insurance sector). Financial institutions will need to develop deeper sustainability bench strength, expanding their capabilities to include management of the environmental impact of their portfolios and, to a lesser extent, their own operations and value chains. And they will have to do so with a structural sustainability skills deficit in the workforce, with the demand for green skills now outstripping supply by a factor of 2:1[1].

With that being the case, financial institutions may have to look to new opportunities to get the needed education. They could take the lead from other industries (e.g. food and agriculture) that have found ways to successfully collaborate to build sustainability depth in their value chains. Asset managers might consider a similarly collaborative approach to educating their portfolio companies by developing customized “climate academies” to help accelerate their portfolio’s transition in a scalable fashion.

Going one step further, as many financial institutions have the same underlying investments, collaboration at the sectoral level with the help of industry bodies would benefit all players. A leaf can be taken out of the playbook developed by the investor group Climate Action 100+ to help businesses transition to a net-zero economy.

Greenhouse gas (GHG) emissions measurement tools and approaches have been improving recently, although challenges remain. Despite that, measurement should be seen as a stepping stone to enable your organization to start taking action. This phrase is becoming a cliche in the GHG accounting sphere, but bears repeating – don’t let perfect be the enemy of good.

The objective of GHG accounting is to identify hot spots in your portfolio to enable prioritization of decarbonization opportunities, in parallel with improving the quality of your GHG data over time. That prioritization could include assessments of which sectors/asset classes/investments in your portfolio you have the greatest amount of influence over, as well as which have the greatest emissions or most reliable data.

With over 150 commercial GHG accounting software tools available, it is imperative to select the best-fit software solution that can help:

- Streamline data collection

- Measure emissions

- Track target-setting, decarbonization initiatives, and emissions reduction progress across a dynamic portfolio

- Integrate with other ESG tools

Carbon removal technologies and permanent carbon storage solutions are critical to achieving societal net zero. Nascent and emerging technologies can present attractive investment opportunities given burgeoning demand, which includes advance market commitments of over $1B from corporate carbon credit buyers. If you are not already familiar with this sector, now is the time to start learning about it.

An integral part of decarbonizing portfolios involves new tools and protocols to enable your organization to screen potential investments in or out, depending on their environmental performance and potential for decarbonization. Private markets firms in particular will have to assess GHG emissions intensities, reduction targets, and transition plans as an essential part of their due diligence process.

One approach is to use temperature rating scores sourced from data aggregators or developing methodologies in partnership with GHG accounting experts. Another approach is to use taxonomies, either existing (e.g., EU taxonomy) or proprietary.

In order to make the net zero transition a Board-level issue, governance structures may also require updates. Below are some examples of measures that financial institutions have been taking:

- Introducing Board-level oversight of processes and controls over GHG measurement as GHG emissions data is starting to make its way into financial statements

- Tying executive compensation to ESG performance, and the same approach could be considered, where appropriate, at the portfolio company level

- Calling on asset managers to incorporate decarbonization and other ESG priorities into their fiduciary duty

Continue to make progress on your climate journey

While these steps can make for a long to-do list, financial institutions should continue to push forward quickly on each of these fronts. With emerging regulation (e.g., new SEC disclosure requirements), global trends like protectionist investment policies, and increasingly clear climate risks and opportunities, financial institutions that fail to act now risk being left behind.

Consultation on FINZ closes on August 14. Please get in touch if you would like to discuss anything that we have covered in this article.

Sources

[1] LinkedIn Global Green Skills Report 2023