The impacts of climate change are so grave and far-reaching that virtually every entity and system on the planet is subject to some form of climate-related risk. Private industry is no exception and is already being confronted with the detrimental impacts of climate change. From the annual devastation of droughts and wildfires, to adverse weather events disrupting shipping and supply chains, to changing policies and consumer preferences, businesses increasingly must calculate climate risks and build long-term strategies to address them.

To further reinforce this concept, earlier this year, the U.S. Securities and Exchange Commission (SEC) proposed a rule change that requires publicly listed companies to include climate-related disclosures in their financial statements and reporting, including disclosure of their greenhouse gas emissions. The implications of the proposed mandate are already causing ripple effects across the private sector. Companies are hypothesizing how the proposal could affect them and educating themselves on how to include climate risk in their strategic planning.

The public comment period for the proposal has been extended to June 17, 2022, and we expect the final rule to change before being brought to the SEC commissioners for approval later this year. For those of you who are catching up on the key pieces of the proposed mandate, in this blog, I’ll summarize what the proposal means for businesses, the main components of the rule, and expected timelines for when these policies might take effect.

SEC proposal aligns corporate climate-related disclosures with investor needs

The proposed rule requires climate-related financial risk disclosures in line with recommendations set forth by the Task Force on Climate-Related Financial Disclosures (TCFD) and greenhouse gas emissions disclosure in line with Greenhouse Gas Protocol’s Corporate Standard to be included in annual SEC filings. A company that knowingly misstates information related to climate-related risk could be subject to criminal penalties. Companies should interpret this to mean that they must take realistic steps to represent their climate-related risk and use reasonable assumptions to develop climate-related risk financial metrics.

Most companies will need to make changes to their climate risk assessment processes and disclosures in response to the SEC reporting requirements. Currently, most companies do not report on climate-related risk in line with all TCFD requirements. The SEC’s analysis of the proposed rule highlights a Moody’s Analytics review of the public filings of 659 US companies in 2020/2021 that found very few included the 11 TCFD disclosures in their public reporting.1

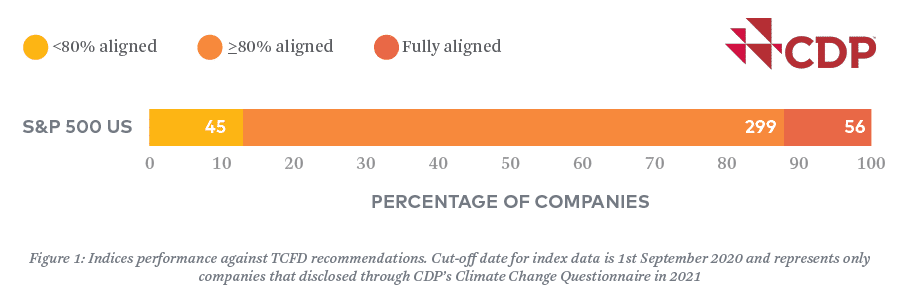

Even companies reporting through CDP’s Climate Change Questionnaire, which has incorporated questions that align responses with TCFD disclosures, will need to step up their reporting. In a review of the 2020 survey (reported in 2021), CDP analysts found that only 14% of S&P 500 companies that reported to CDP achieved 100% TCFD-aligned disclosure. An additional 74% were at least 80% aligned with TCFD.2

The introduction of TCFD-aligned reporting requirements by the SEC will significantly improve corporate and investor awareness of climate-related risks and enhance the resilience of investment portfolios. The TCFD is composed of companies that both prepare and consume financial disclosures. The recommendations are designed to guide companies toward meaningfully integrating climate change into their business planning and strategy development. The associated disclosures provide decision-useful climate-related data for investors, lenders, and others. They make it clear which companies are prepared to succeed in the transition to a net-zero economy.

Qualitative climate-related risk and planning disclosure requirements

|

Transition risks are risks related to a potential transition to a lower-carbon economy on business and profitability. Examples: Increased costs attributed to changes in law or policy, decreased sales, prices, or profits for carbon-intensive products as a result of lower market demand, the devaluation of assets, etc. |

|

Physical risks refer to potential harm to businesses and their assets arising from acute climate-related disasters, Examples: wildfires, hurricanes, tornadoes, floods, and heatwaves as well as chronic risks, which refer to more gradual impacts. Examples: long-term temperature increases, drought, and sea-level rise. |

|

Transition risks are risks related to a potential transition to a lower-carbon economy on business and profitability. Examples: Increased costs attributed to changes in law or policy, decreased sales, prices, or profits for carbon-intensive products as a result of lower market demand, the devaluation of assets, etc. |

|

Physical risks refer to potential harm to businesses and their assets arising from acute climate-related disasters. Examples: Wildfires, hurricanes, tornadoes, floods, and heatwaves. Chronic risks refer to more gradual impacts. Examples: Long-term temperature increases, drought, and sea-level rise. |

The proposed mandate requires companies to accurately and comprehensively assess and report on their climate-related risks and accompanying plans. The following information is included in the description of climate-related risks:

- A description of both transition risks and physical risks, and how the risks will play out over the short-, medium-, and long-term.

- A description of the actual or potential impacts of climate risks; a description of whether and how these impacts are considered as part of the company’s business strategy, financial planning, and capital allocation; and a description of how the risks are likely to affect the line items of the company’s consolidated financial statements.

- A description of the resilience of the company’s business strategy considering potential future changes in climate-related risks.

- If the company has an internal price on carbon, disclosure of specific information about the price, including whether and why different prices are used in different circumstances.

- If the company undertakes climate scenario analyses, details on this process, and the use of the analyses.

- Climate-related risk management processes

The company must describe any processes for identifying, assessing, and managing climate risks. If applicable, it must describe its transition plan to address specific focus areas outlined in the rule. - Disclosing established climate targets and related progress

If the company has climate targets, including greenhouse gas reduction targets, it must disclose the targets and progress made towards the targets. This includes reporting on specific details about targets or goals that have been set, the data used to measure progress towards the goal, and details (e.g. source, location, registry, and cost) on any purchases of renewable energy certificates (RECs) or carbon credits.

Mandatory reporting of GHG emissions

- All companies must disclose scope 1 and scope 2 emissions. These emissions must be disclosed separately in three forms: (1) total greenhouse gas emissions in each scope, disaggregated by constituent greenhouse gas and in the aggregate in carbon dioxide equivalent; (2) greenhouse gas intensity per unit of total revenue; and (3) greenhouse gas intensity per unit of production relevant to the industry.

- A company must disclose scope 3 emissions if the emissions are material or if the company has a target covering scope 3 emissions, with the exception that small companies do not need to disclose scope 3 emissions. If required, scope 3 must be reported in the three forms described above.

- Large filers and accelerated filers are required to submit an attestation from a greenhouse gas attestation provider for the calculation of their scope 1 and scope 2 emissions. This requirement is phased in several years after a company first submits an emissions disclosure.

Climate-related financial statement metrics and disclosures

Three categories of climate-related financial metrics are required to be included in a company’s audited financial statements: financial impact metrics, expenditure metrics, and financial estimates and assumptions. This includes the financial impacts of the physical and transition risks identified by the company, expenditures related to mitigating these risks, and the financial estimates of transition activities. These metrics and disclosures are subject to the company’s financial statement audit requirements.

The future of climate-related disclosure and resiliency planning

This preliminary proposal gives us a sense of what information investors seek in order to make informed decisions on the impact of climate change on their investments. We expect the SEC to receive significant comments on the proposed rule, both from those in favor of increasing the stringency of rules and from those opposed to the requirements. It is not clear where the final rule will land or what is a reasonable timeline for adoption. The earliest the rule could apply to any company is in 2024 for fiscal year 2023 reporting.

It is clear, regardless of the final details of the SEC mandate, that investors expect companies to take meaningful measures to integrate climate impact analysis and resiliency planning into their operations and company strategy. Incorporating related disclosures into annual financial filings will safeguard investments and provide critical information on what companies are doing to assess and mitigate climate-related risk. 3Degrees will remain at the forefront of SEC proposal developments and will follow up with noteworthy updates as they become available.

For questions on how your organization can begin preparing for the pending SEC climate-related disclosure mandate contact us.

Resources:

1How the CDP is aligned to the TCFD – CDP.net

2 Moody’s Analytics webpage; (SEC proposal summary table on p.315)