The ambition of fit-for-purpose and fit-for-future

As we anticipated in our last European Renewable Markets Insight Report, the EU electricity market is about to undergo significant regulatory changes. The proposed reform package presented earlier this year shows how the European Commission (EC) is aiming to better protect consumers and integrate renewables in the energy system as a result of the energy crisis we have experienced since the war in Ukraine started. Our analysis has mostly focused on the proposed long-term solutions, in particular the encouragement of implementing Power Purchase Agreements (PPAs) among EU Member States and the necessary measures toward that direction.

After presenting the proposed reform package, the EC passed it by the European Council and European Parliament (EP) for debate and negotiation. On September 14th, the EP formally adopted a position, with each political group providing comments and improvements to the text. In the following sections, we’ll be evaluating the amendments related to the articles that promote the implementation of long-term solutions like PPAs, namely:

Article 9: Forward Markets

Article 9: Forward Markets- Article 19a: Power Purchase Agreements (PPAs)

- Article 19ab: Union PPA Database

- Article 19ac: Voluntary Standardized PPAs

Article 9: Forward Markets

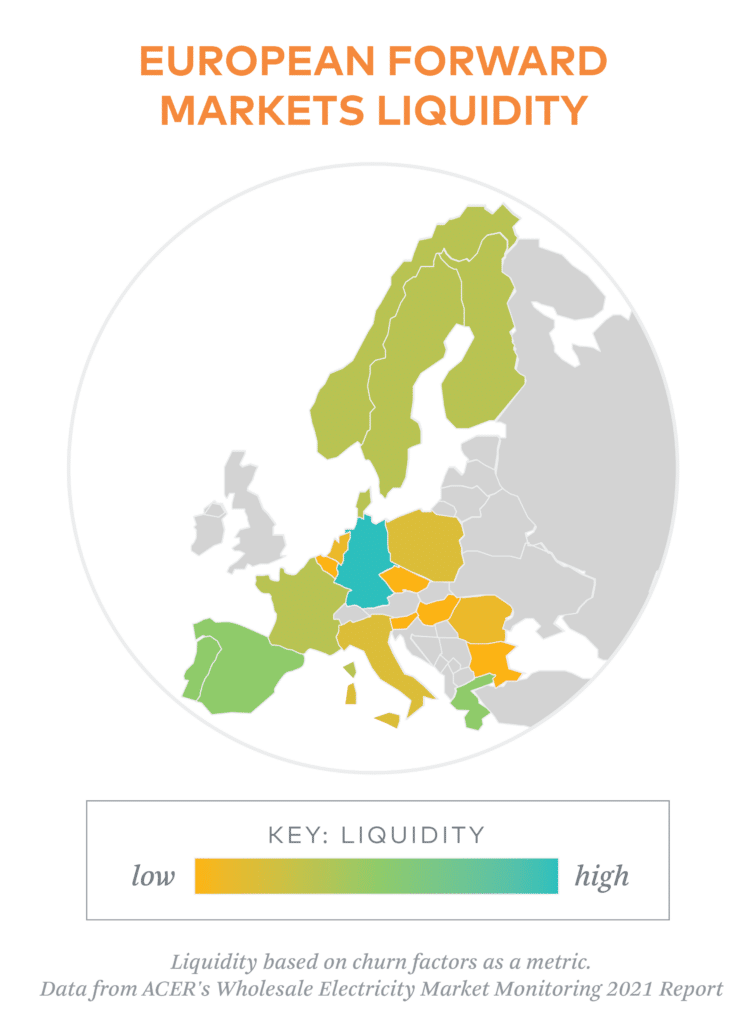

The capability of implementing long-term solutions, such as hedges and PPAs, is linked to the liquidity of the forward electricity market in each bidding zone. Currently, with the exception of the Nordic region (Finland, Sweden, Norway and Denmark), each zone is a stand-alone market, leading to a fragmented and unequal distribution of liquidity, with Eastern countries being a clear example of a lack of liquidity compared to Western and Central Europe and the Nordics. To address this issue, the EC has proposed the implementation of virtual hubs that would pool all bids and offers on forward contracts in a region, boosting liquidity and creating a single reference price for several countries.

The EP has since provided several amendments to Article 9, primarily asking for a submission of a specific assessment on the impact of the regional hub establishment (with a direct focus on underlying benefits and drawbacks of such implementation compared to the existing zonal model). In addition, the amendment urged that the EC should define specific situations where bidding zones may belong to two or more virtual hubs, including an indicative implementation process of the new hubs.

Article 19a: Power Purchase Agreements (PPAs)

In article 19a.1, the EC has clearly indicated that EU Member States should facilitate the development of PPAs in order to achieve the decarbonization targets set in Article 4 of Regulation EU 2018/1999, which targets the achievement of at least 32% renewable energy by 2030 and now increased to a minimum of 42.5% (aiming for 45%) under the Renewable Energy Directive (RED) III. In their amendments, the EP has underlined that in order to ensure the removal of barriers to PPAs, the EC needs to provide specific guidelines on how to alleviate administrative obligations and accounting complexities, which are generally key obstacles for corporates wanting to enter into a PPA contract.

Financial risks associated with the potential for buyers to default on payment obligations also play an important role in PPA negotiations, thus making it difficult for non-creditworthy buyers to find a counterparty. The EC is well aware of how this challenge results in a clear obstacle for the growth of PPAs, as this currently makes them an opportunity suited only for specific corporations. Therefore, EU Member States will likely be asked to coordinate with the European Investment Bank (EIB) or other Union-level facilities to provide, for example, guarantee schemes to targeted customers, such as micro enterprises, small and medium-sized enterprises (SMEs), households, as well as aggregators, renewable energy communities and others.

As a consequence, we expect demand for PPAs to increase considerably, especially through aggregation due to the establishment of a voluntary market platform for PPAs. Developed in collaboration with Nominated Electricity Market Operators (NEMOs), the platform is expected to be in operation by the end of 2024.

Article 19ab: Union PPA Database

The EP introduced a completely new section to Article 19, which focuses on the development of an EU database that would collect and monitor relevant information on signed PPAs. In the EU, there is currently no established system for monitoring signed deals between sellers and off-takers, and all information related to PPAs is announced by the parties on a voluntary basis. What the EP is proposing can be compared to the Clean Energy Buyers Association (CEBA) deal tracker in the United States, which tracks the total annual volume of clean energy procured by energy buyers, as well as companies that have made clean energy procurement announcements since 2014.

In addition, the EP leaves the possibility of creating similar databases on a national level for EU Member States, with the aim of publishing an annual report on the PPA market in order to monitor the growth. The responsibility for setting up, maintaining and managing the EU database would rest with the Agency for Cooperation of Energy Regulators (ACER). The database would also allow ACER and National Regulatory Authorities (NRAs) to collect the necessary information for monitoring and issue reports on how this market segment is functioning.

In terms of the timeline, the EU database is expected to be operational within 12 months after the amended Regulation enters into force.

Article 19ac: Voluntary Standardized PPAs

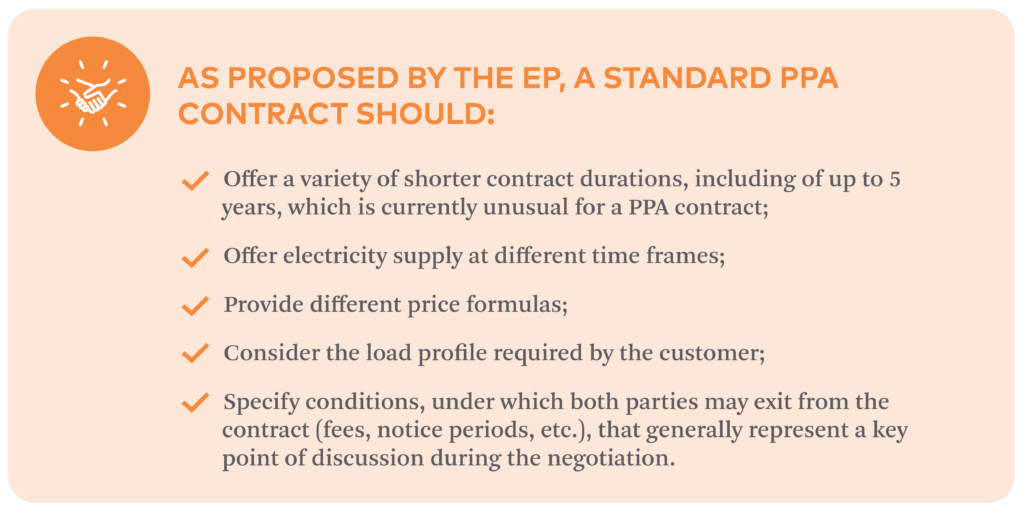

In line with the main goal of removing barriers to PPAs, the EP has proposed the development of standardized PPAs used on a voluntary basis by the contracting parties. The contracting process is generally long and tedious, as both parties need internal alignment with different departments and must find agreement on controversial clauses, which are often country-specific. PPA contract negotiations end up being a significant barrier for buyers, especially the smallest ones that are unable to allocate such resources to contracting and struggle to accommodate specific PPA requirements and obligations. The EP generated a list of characteristics that a standard PPA contract should follow.

Next Steps for EU Market Design

In July, Spain succeeded Sweden in the presidency of the European Council for a 6-month period. The ambition is that an agreement on the market design reform will be reached before the end of the year.

At this point, the most contested point relates to direct price support schemes for new investments in electricity generation, with countries being concerned about the impacts of providing subsidies to existing projects in the form of Contracts for Difference (CfDs). Germany, Austria and Luxembourg have warned this could distort the EU market by giving some states a competitive edge (e.g., France with the potential use of these subsidies for its nuclear fleet).

The end of year target to reach an agreement is tight, considering the political uncertainty that Spain is currently facing after its election in July, as the political parties have very different ideas about climate and energy. Furthermore, the current EP will dissolve before June 2024, thus adding pressure for Members to finalize their positions before the deadline.

3Degrees will keep monitoring the developments and cover the most crucial ones in the upcoming edition of our European Renewable Markets Insight Report. In the meantime, please reach out to our team for a chat about European energy markets.

Recent Comments