![]()

![]()

As part of their journey to reach a 2050 goal of net zero greenhouse gas emissions, Mondelēz International, a global snacking company, has been working towards its aim to reduce its scope 2 footprint worldwide. With a short-term target of reducing their absolute end-to-end GHG emissions by 10% by 2025, relative to a 2018 baseline, they set their sights on Poland, where they could aim to make a meaningful contribution to emissions reductions in a carbon-intensive country.

Mondelēz International approached 3Degrees to develop and implement a renewable energy procurement strategy to help address emissions from electricity consumption in its Polish manufacturing facilities.

Challenges

- In 2022, Europe faced unprecedented market volatility, with rising energy costs that made renewable energy developers hesitant to enter into long-term corporate power purchase agreements (PPAs). This resulted in limited project supply to meet corporate demand;

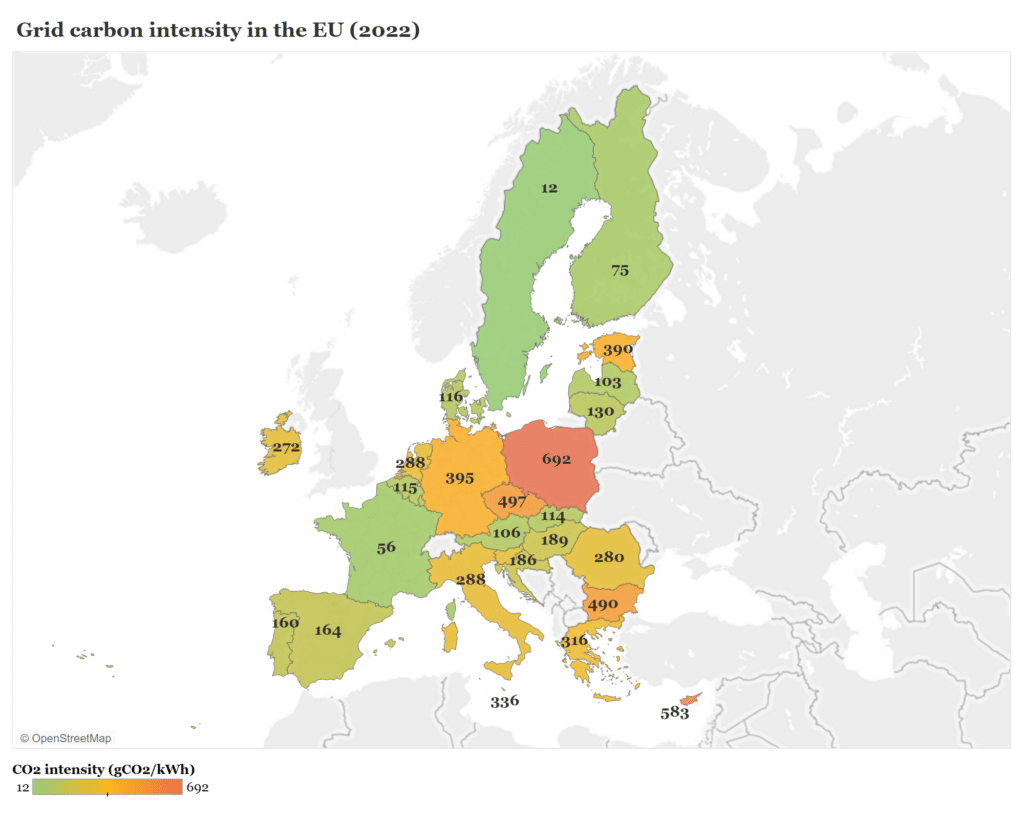

- Mondelēz International needed a project that would aim to reduce its greenhouse gas footprint across its growing portfolio of production plants in Poland;

- Ever-changing market conditions made it difficult to keep stakeholders up-to-date and educated on the process throughout. This was especially challenging as PPA prices continued to increase rapidly over short time periods.

How we helped

3Degrees worked with Mondelēz International to facilitate workshops to educate and align stakeholders on the current state of European energy markets and PPAs. Based on the input and feedback gathered in these workshops, the 3Degrees team was also able to determine the best-fit project characteristics to meet Mondelēz International’s needs and preferences.

With this information, 3Degrees developed a tender strategy and, upon Mondelēz International’s approval, issued a Request for Proposals, which included:

Financial modeling to estimate each offer’s projected Net Present Value (NPV), monthly cash flows, and implied guarantee of origin (GO) value;

Conducting comprehensive market development and contractual risk analyses;

Evaluating each project according to Mondelēz International’s criteria, specifically, geographic location, technology, development maturity, and counterparty qualifications.

Once Mondelēz International selected a project, 3Degrees supported the PPA contract negotiation process.

Results

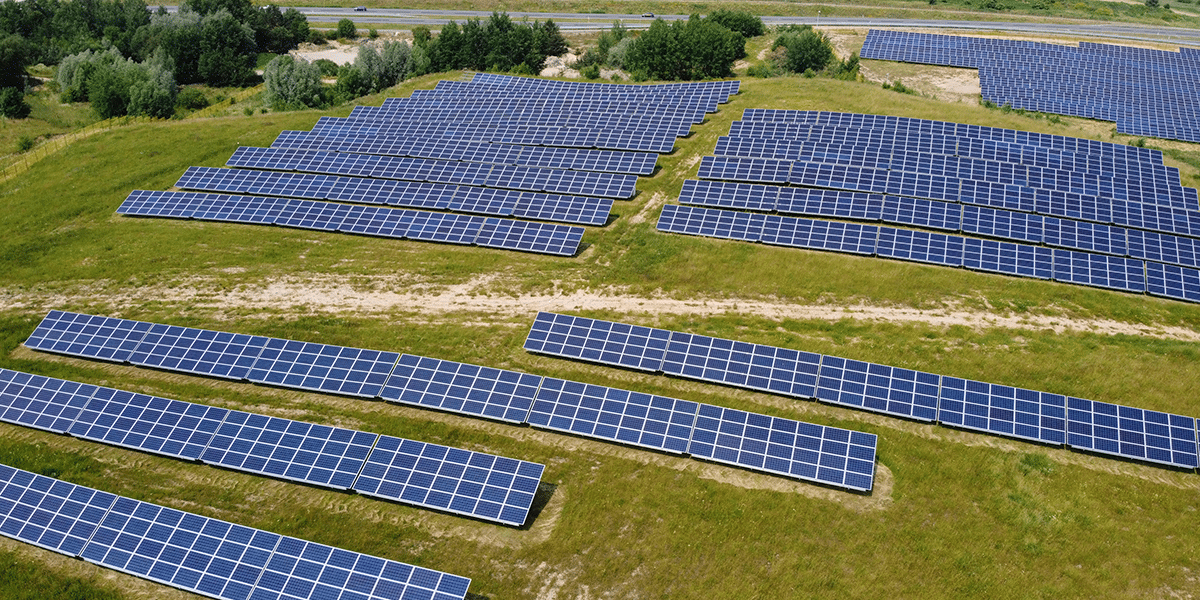

Mondelēz International signed a 12-year PPA with a renewable energy developer in Poland for approximately 126 GWh of solar electricity. The project aims to enable Mondelēz International to:

- Displace more than 1 million metric ton equivalent of CO2 emissions from electricity generation during the PPA term, which will contribute to reaching 40% of its carbon reduction goal in Europe;

- Achieve its goal of covering its annual Polish electricity consumption with GOs produced within Poland.

As part of our ongoing advisory support, 3Degrees will provide PPA monitoring services to Mondelēz International in order to evaluate project performance and incorporate the Poland PPA into its European renewable electricity portfolio.

“At Mondelēz we are as ambitious about sustainability as we are in chocolate making. We are very happy to work with 3Degrees who shared our ambition at a time when Europe was going through the biggest energy crisis since WW2. Several times we experienced the advantage of working together as we adapted our reach to the market and used your expertise in our tough negotiations.”

— Ilkem Yildiz , Sourcing Manager, Energy & Utilities Europe, Mondelez International

“Mondelēz International’s achievement of its ambitious goal in Poland is an excellent example of a corporate buyer making the maximum possible impact through project selection in a carbon intensive grid. We are thrilled to have supported Mondelēz in signing a 12-year PPA in Poland despite challenging market conditions, which is a testament to Mondelēz’s tenacity and a significant climate action milestone in Europe.”

Average emissions method:

Average emissions method: Marginal emissions method:

Marginal emissions method:

Recent Comments