The EU has set its sights on carbon removal projects. Developing local carbon sequestration capacity and market trust through harmonisation and transparency is the central aim of the Proposal for Establishing a Union Certification Framework for Carbon Removals recently adopted by the European Commission (EC).

This shouldn’t come as a surprise considering EC’s rollout of the European Green Deal in 2019, which outlines a vision to reach carbon neutrality as a continent by 2050. This feat will require not only dramatically reducing most of its greenhouse gas emissions year after year but significantly scaling up atmospheric carbon removal, required to balance out hundreds of millions of tons of residual, hard-to-abate CO2 emissions.

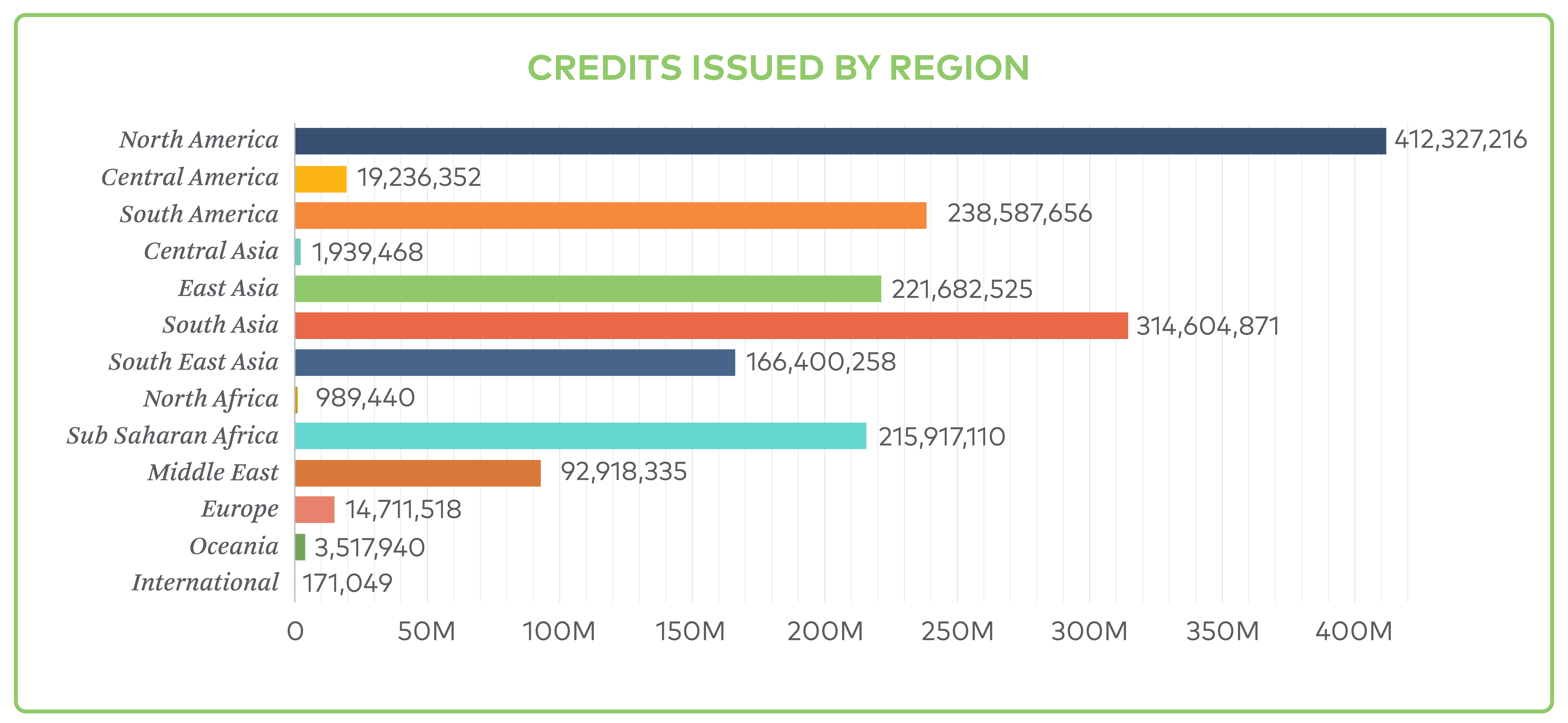

To date, relatively few carbon projects have been developed on the continent. As of December 2022, less than 1% of all carbon projects listed by four major voluntary offset project registries are located in the EU (see image 1). The Union’s latest move hopes to change that by spurring investment and trust in local carbon removal.

It is expected that more carbon removal credits from local projects will become available and procurement more streamlined once a robust network of third-party verifiers and standardised quality criteria is established.

Image 1: Berkeley Carbon Trading Project’s Voluntary Registry Offsets Database. Version 7 contains all projects, issuances, and retirements through 31 December 2022

Current scenario with carbon removals

While projects that can remove atmospheric carbon already exist, they are still unavailable to most market participants due to high cost, limited supply, and uncertainty around nascent technologies. Despite these factors, leading standard-setting bodies such as SBTi still assert that carbon removals are the only way to neutralise residual emissions.

Even though removal technologies such as direct air carbon capture (DACC) have been around for years, the entire removals market is still in its early stages. Most operating projects still fall into the avoidance or reduction categories. According to Carbon Direct, only 3% of projects exclusively issued removal credits in 2021, while 13% issued a mix of removal and reduction credits. Why?

In spite of these concerns, demand for carbon removal is expected to grow, driven by a variety of pressures coming from investors, consumers, and legislation. To bridge the gap, massive investment is needed.

Europe’s steps toward a reliable carbon removal market

EC’s adoption of the first EU-wide voluntary framework to reliably certify high-quality carbon removals is an ambitious move. It serves as a foundation to build the carbon removal equivalent of the EU’s integrated framework for issuing, holding and transferring Renewable Energy Guarantees of Origin (GOs).

Today, GOs are bought, sold, and retired to make reliable decarbonisation claims in a relatively straightforward process due to a system that guarantees credit quality, comparability and security for both renewable project developers and GO buyers. This environment has boosted unprecedented investment in renewables, adding record capacity to the European grid. The European Union is hopeful the same can be achieved with carbon removals in the near future.

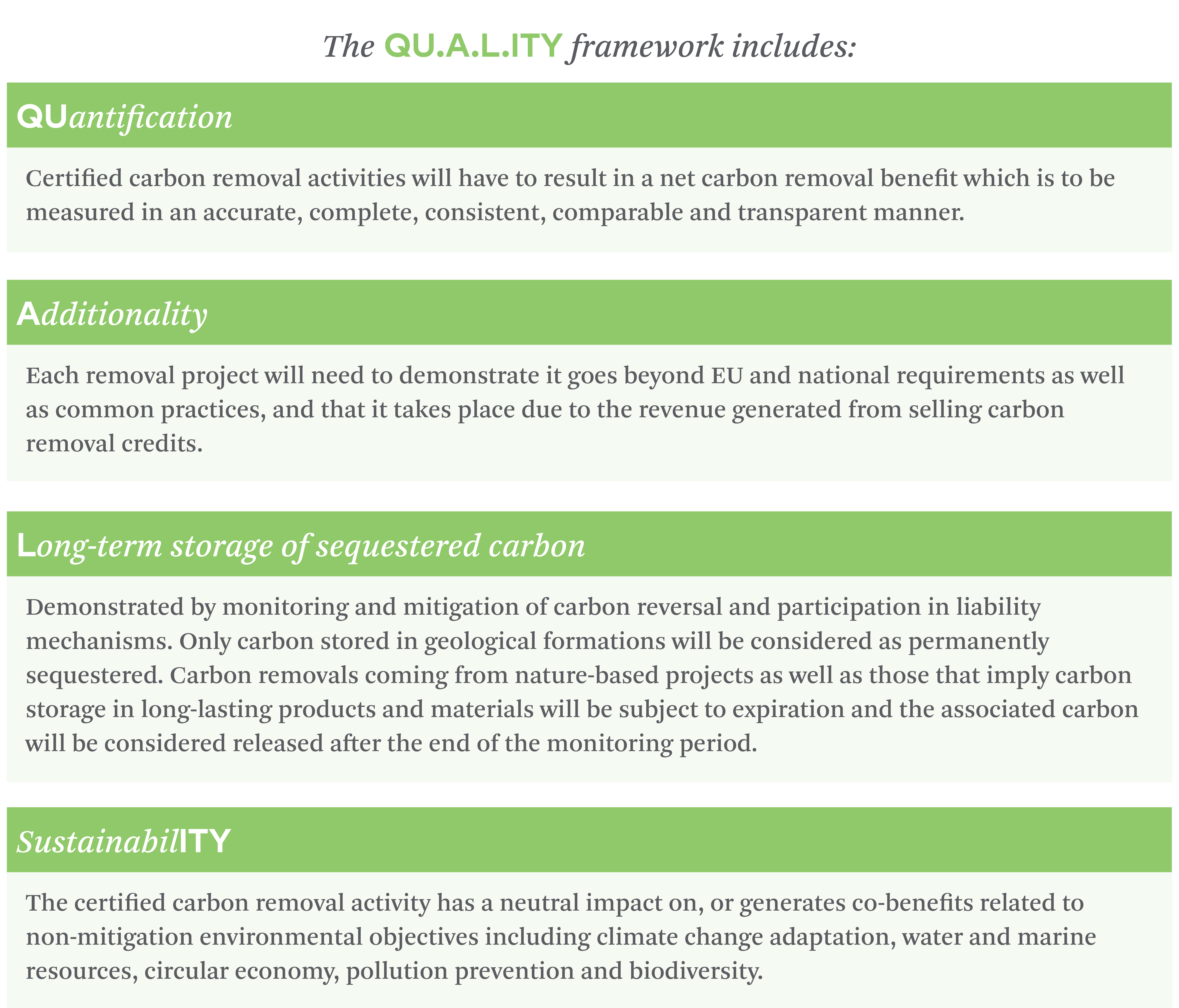

The framework aims to increase the level of trust in the European carbon removal market. Establishing a standardised certification system across member states is expected to attract developers and increase local carbon removal capacity and supply of high-quality removal credits. More precisely, a network of third-party verifiers will ensure that carbon removal credits entering the voluntary market align with the quality criteria laid out in the framework under the acronym QU.A.L.ITY.

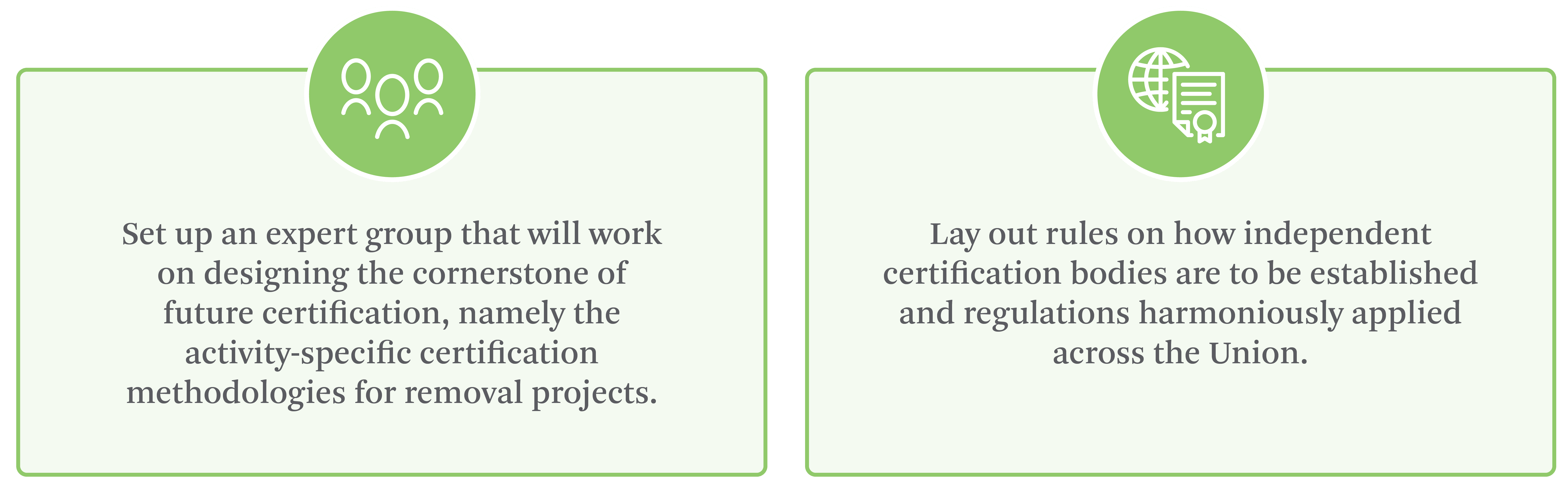

Before it can be implemented across the EU, the framework will need to be discussed and adopted by the European Parliament and the Council. True execution of this ambitious plan, however, will have to wait until its key building blocks are developed. Furthermore, the European Commission will need to:

It is only then that carbon removal projects will be able to apply for EU certification. These projects will need to be audited in order to verify compliance with the QU.A.L.ITY criteria before credit issuance. The compliant EU-certified credits will be registered in a public registry to make all relevant information publicly available, thus reducing the risk of double-counting.

The success of this framework will depend on the thoroughness and accuracy of the methodologies that have yet to be put forth, as well as the integrity of the future certification system and its checks and balances.

What would the EU carbon removal certification system mean for carbon procurement?

If successful, an EU-wide carbon removal certification system will minimise the risk of greenwashing by way of harmonised enforcement of the QU.A.L.I.TY criteria across all member states. Today, procurement can be a heavy lift for corporates. Removal projects remain sparse, technologies new, and depending on how companies choose to contract for removals, delivery volumes may be uncertain.

Some removal credits—particularly those from technology-based projects like DACC—are extremely expensive, and many of the potential quantification approaches are still under development. This is why much of carbon removal procurement activity today is led by market pioneers like Microsoft, Google and Meta, who are able to make substantial investments in nascent technologies.

For the European Union to achieve its carbon-neutral goal, the removals market must grow and mature to accommodate a greater number of purchasers. The adoption of the EU framework is one key step to scaling the removals market and providing buyers with essential quality assurances, but it is only the first of many required steps.

Ensuring quality, market transparency, and a healthy supply of removal credits at an attractive price isn’t going to happen overnight, but once a reality, the established market will have the potential to streamline procurement and make carbon removals more accessible to corporates looking for impactful climate action.

Conclusion

It will take time before carbon removal credits are as accessible as credits coming from reduction and avoidance projects. The EU, however, seems to be very aware of the challenges it faces on the road to net zero and has chosen regulation at the foundation of its local carbon removal market.

The Proposal for Establishing a Union Certification Framework for Carbon Removals is not a fully developed solution but rather an important first step towards increasing the supply of EU-based carbon removals while standardising credit quality and simplifying procurement.

The age of carbon removals is ramping up, and Europe is determined not to fall behind. 3Degrees continues to support clients in navigating the uncertainty in this rapidly changing market landscape.

Recent Comments