In early November, I met up with several 3Degrees team members from around the globe at the first I-REC Standard Conference (ISC) in Bangkok, Thailand, to discuss the expansion of renewable energy markets worldwide. It was stimulating to engage with so many industry peers from more than 30 countries to discuss a common topic: standardizing global attribute markets to all regions. Asia is often seen as the next frontier, with much interest from companies, governments, market actors, and other stakeholders in the region’s renewable energy expansion, so it was especially fitting to be meeting in Thailand.

The fully-packed schedule provided insights into different topics related to the expansion of access to renewable energy instruments. At the end of a whirlwind two and a half days, I came away with a few key takeaways.

Need for Global Standardization with Local Implementation

Several sessions focused on the theme of “global standardization with local implementation.” In other words, there’s a need for standardizing the process of issuing, transacting, and retiring energy attribute certificates (EACs) worldwide – a practice recognized by companies, governments, advocacy organizations, supply chain partners, and even the general public as proof to back up environmental claims.

However, regulatory and structural differences in national and regional energy markets will require collaboration with local governments to establish systems and processes to allow the sale of international RECs (I-RECs). Consequently, promoting local issuance of I-RECs brings confidence to renewable energy procurement, helping companies meet their voluntary climate commitments and driving investments in the market.

In a nutshell, the introduction of the I-REC system in a new country can be a significant driver of new renewable energy development, making it an attractive market for companies to operate in.

Use of Renewables Across the Supply Chain

Hans Goetze from Lock23, Julie Casabianca from 3Degrees, and Valerie Choy from Amazon Web Services discussing “Use of Renewables across the Supply Chain” at ISC 2022. Image courtesy from the International REC Standard

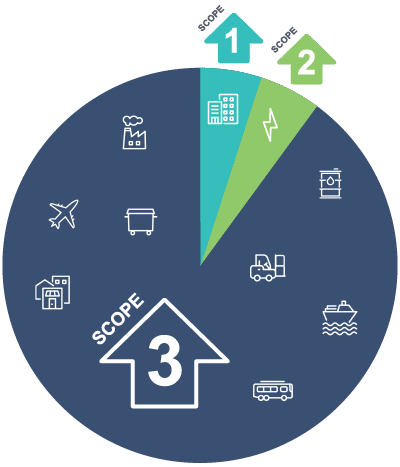

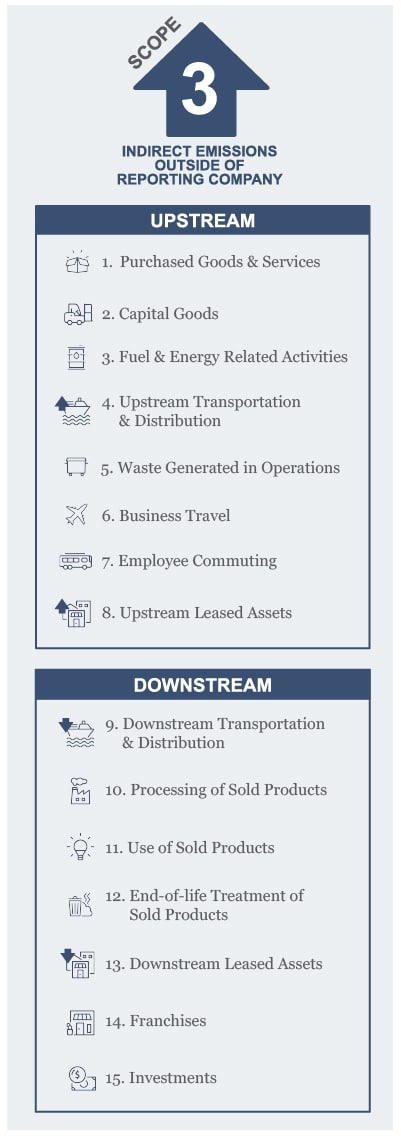

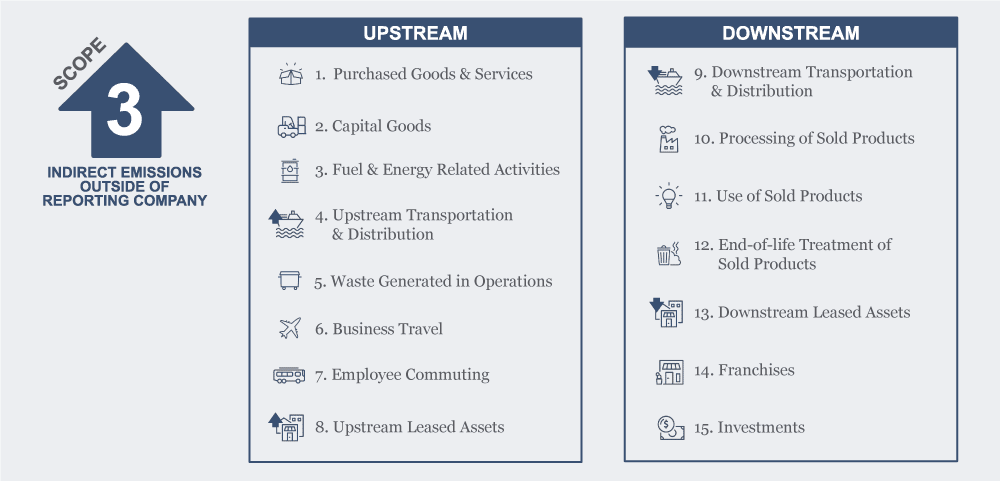

I had the pleasure of presenting on the panel: “Use of renewables across the supply chain”, where the central theme was how organizations are increasingly taking steps to address their supply chain emissions, also known as scope 3 emissions. The panel also discussed emerging solutions for linking a supplier’s scope 2 emissions to a reporting company’s scope 3 accounting.

In setting the scene, I reviewed the drivers and trends in supply chain decarbonization and outlined how addressing electricity use in the supply chain can be an effective way to make material reductions in companies’ scope 3 emissions. However, doing so poses a number of challenges:

- Difficulty getting actionable, primary energy use data from suppliers

- Meaningful engagement with suppliers requires time

- Lack of robust guidance on reporting scope 3 electricity emissions

- Limited guidance on direct action opportunities for reporting companies

- Limited renewable electricity procurement options in some markets

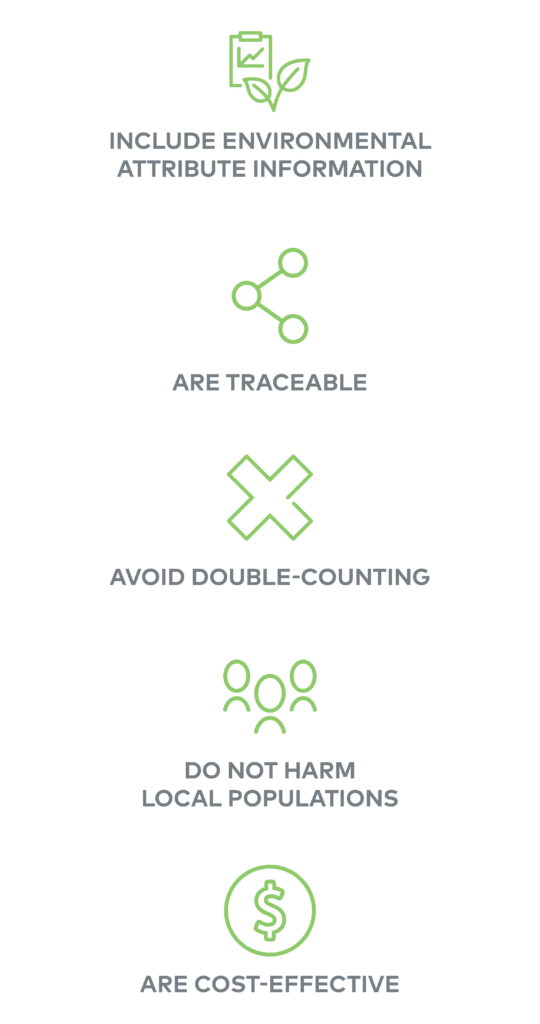

It’s important to remember that one organization’s electricity-related scope 3 emissions are another’s scope 2 emissions. Just as reporting companies need options for their claims, suppliers need appropriate renewable electricity options to procure in their local markets, and these options may currently be limited. Utilities and power producers can drive new market opportunities by developing products that help companies reach their climate targets for organizations such as RE100, SBTi, and CDP, and meet the following criteria:

Companies can work with the I-REC Standard Foundation and various industry groups to help advocate for government policies that expand the available options for all energy consumers.

Tracking Developing Trends

Other trends addressed at the conference relate to emerging changes in energy markets and how these changes are expected to impact corporate energy buyers.

- From voluntary emissions reporting and reductions to increased regulation and requirements. Several speakers highlighted this theme, which is exemplified in the U.S. Securities and Exchange Commission’s proposed rule change for corporates to include climate-related disclosures in their financial statements and reporting and the EU’s proposed Carbon Border Adjustment Mechanism (CBAM). There was a common interest in understanding how this shift would impact companies’ and governments’ renewable energy deployment.

- Update on the GHG scope 2 guidance: With an eye to the anticipated GHG Protocol updates, it was valuable to have robust discussions about what makes impactful procurement and how market-based instruments like I-RECs are essential to a functioning renewable energy market.

- From operation-level electricity reductions to product-level tracking of carbon emissions released with the production of a product: In Europe, the CBAM aims to prevent carbon leakage by requiring importers to quantify emissions associated with imported materials and pay a fee on emissions released during the production process of certain carbon-intensive goods. A reporting system for those goods would apply from 2023 and from 2026, importers are expected to begin paying the financial adjustment. Discussions highlighted how EAC systems could support credible electricity emissions accounting for products, if required to be included, allowing companies to better understand and control the embodied emissions of their products. While the European Parliament, Commission and Council have varying positions on the regulation, negotiations on CBAM implementation are set to be completed by the end of the year.

- 24/7 and hourly EAC matching: Speakers shared how innovative platforms and tools are enabling more granular tracking and matching of electricity products, allowing companies with this ambitious goal to purchase renewable electricity that is produced at the same hour of each day that they are consuming electricity. Others cautioned that this market evolution should not come at the expense of disruption to the market or restrictions for other companies, particularly those just entering the EAC markets. A shared feeling among participants is that we need to provide standard instruments in markets that increase accessibility for all companies.

The conference demonstrated that demand for renewable energy and, in turn, EACs is growing, particularly in international markets, as companies look to reduce their own emissions, their supply chain emissions, and their product-level emissions. Expanding access to trusted, standardized instruments, like I-RECs, in markets worldwide will help companies reach their goals and drive the global sustainable energy transition. I feel honored to have joined other market leaders, as well as new market participants, at the first I-REC Standard Conference 2022, and I look forward to continuing the discussions at next year’s conference in the UAE.

If you’ve got a question or need assistance with your organization’s renewable energy procurement or supply chain strategy, don’t hesitate to get in touch.

As EV technology has reached fleet-capable vehicle classes including pickups and vans, and local, state, and federal incentives continue to scale, companies around the world are assessing when and how to transition to electric fleets in order to accelerate progress toward overarching climate targets and bring down total cost of ownership.

As EV technology has reached fleet-capable vehicle classes including pickups and vans, and local, state, and federal incentives continue to scale, companies around the world are assessing when and how to transition to electric fleets in order to accelerate progress toward overarching climate targets and bring down total cost of ownership.

Recent Comments